The Smart Way to Save: How FinTech is Automating Your Financial Future

It wasn’t that long ago that managing your money felt like a chore. We’d sit down with stacks of bank statements, spreadsheets, or maybe even those old-school paper envelopes, trying to track every dollar and figure out how to squeeze out some savings. The world of personal finance seemed complex, often intimidating, and definitely time-consuming. But thanks to FinTech – financial technology – that paradigm has dramatically shifted.

The Evolution of FinTech for Everyday Consumers

We’ve seen rapid advancements transforming everything from money management to investing and even how we transfer funds. Gone are the days when sophisticated investment tools were only for the wealthy or finance professionals. Today, a new wave of digital apps and online platforms has emerged, simplifying these crucial financial tasks and, perhaps most importantly, promoting automated savings. These innovations are changing the way we interact with our money, making it more accessible and manageable for everyone.

The core concept driving this change? Effortless savings through automation. FinTech apps are designed to help you save without constant, active effort on your part. My take is that these applications leverage smart technology to integrate savings seamlessly into your daily life, making those big financial goals – whether it’s building an emergency fund, saving for a house, or planning for retirement – feel much more attainable.

The Mechanics of Automated Saving: “Set and Forget” Strategies

So, how do these apps work their magic? It’s all about “set and forget” strategies that tap into both technology and human psychology.

Psychological Benefits of Automation

One of the biggest hurdles for many of us is simply starting to save or sticking to a plan. Automation helps overcome this “saving inertia” and procrastination. By setting up consistent financial habits, these tools reduce the mental load and financial stress often associated with manual budgeting. You’re essentially building a disciplined approach to money management without feeling like you’re constantly micromanaging your money. It creates a positive feedback loop, leading to better financial health over time.

Key Automated Mechanisms

FinTech apps employ several clever mechanisms to make saving effortless:

- Rule-Based Automatic Transfers: Many apps allow you to define custom rules for transferring funds to savings. Think of it like a personalised financial game. For instance, Qapital offers “Guilty Pleasure” rules that let you save a small amount every time you indulge in a specific habit. You can also set up scheduled transfers, like a fixed percentage of your income every payday, making sure you “pay yourself first.”

- Spend Round-Ups: This is a popular way to save small amounts. Apps like Acorns and Chime automatically round up your purchases to the nearest dollar, with the difference transferred to a designated savings account or investment portfolio. It’s a prime example of how small, consistent contributions can accumulate significantly over time.

- AI-Driven Financial Intelligence: This is where it gets really smart. Algorithms analyze your spending patterns and income to identify safe amounts for transfer without risking an overdraft. Oportun (formerly Digit), for example, excels at this, helping prevent overdrafts by intelligently moving money. Other apps like Mint and SoFi use AI to provide personalised advice and nudges based on your unique financial behaviour.

- Consolidated Financial Overview: Having all your financial accounts—checking, savings, credit cards, investments—in a single, intuitive interface can significantly improve financial decision-making. Platforms like Mint and Meniga (a European FinTech firm) aggregate this data, offering a clear picture of your financial health. Research cited in the Review of Finance* highlighted by Rice Business found that Meniga app users saw non-sufficient funds (NSF) fees drop by a remarkable 38.4% within two years of adoption, simply by having better visibility into their money.

Exemplary FinTech Applications for Automated Savings

The FinTech Market is brimming with innovative apps designed to make saving and investing easier. Here are some top players across different categories:

Platforms for Automated Saving & Micro-Investing

Oportun App – Automated Savings & Overdraft Protection

- Oportun: Known for its intelligent automated savings, proactively helping you avoid overdrafts.

Oportun is a financial app designed to help users build savings automatically while protecting against costly overdrafts. Here’s what you need to know about its key features.

Pros of Oportun

Smart Automated Savings: Oportun uses intelligent algorithms to analyze your spending patterns and automatically set aside small amounts you won’t miss. This “set it and forget it” approach helps users build emergency funds without manual transfers.

Proactive Overdraft Prevention: The app monitors your account balance and upcoming bills, alerting you before potential overdrafts occur. This feature can save users significant money in overdraft fees, which average $35 per incident at traditional banks.

Hands-Free Money Management: Once configured, Oportun works in the background, requiring minimal user intervention while building financial cushions over time.

Cons of Oportun

Limited Control: Automated systems may not account for irregular expenses or sudden financial changes, potentially moving money when you actually need it accessible.

Requires Bank Linking: Like most fintech apps, Oportun needs access to your bank account data, which may concern privacy-conscious users.

Subscription Costs: Many automated savings apps charge monthly fees that can add up over time, potentially offsetting some savings benefits.

Not a Complete Solution: While helpful for overdraft prevention, the app doesn’t replace comprehensive budgeting or address underlying spending issues.

Bottom Line

Oportun works best for individuals who struggle with consistent saving habits and frequently face overdraft risks. However, users should weigh subscription costs against potential savings and consider whether automated features align with their financial management style.

Acorns App – Spare Change Investing & High-Yield Savings

- Acorns: Invests your spare change through round-ups into diversified portfolios and now offers features like high-yield deposit accounts.

Acorns is a micro-investing app that automatically invests your spare change from everyday purchases into diversified portfolios. With added high-yield deposit accounts, it’s become a comprehensive platform for building wealth effortlessly.

Pros of Acorns

Effortless Round-Up Investing: Acorns rounds up every purchase to the nearest dollar and invests the difference. Buy a $3.50 coffee, and $0.50 goes into your investment portfolio. This painless approach helps beginners start investing without large upfront capital.

Diversified Portfolios: Your spare change is invested in ETF portfolios designed by financial experts, providing instant diversification across stocks and bonds based on your risk tolerance.

High-Yield Deposit Accounts: Acorns now offers competitive savings rates, allowing users to earn significantly more than traditional bank accounts while keeping emergency funds accessible.

Educational Resources: The app includes financial literacy content, helping users understand investing fundamentals while they grow their money.

Low Barrier to Entry: No minimum investment required—you can start building wealth with just pennies from your daily transactions.

Cons of Acorns

Monthly Subscription Fees: Acorns charges $3-$12 monthly depending on the plan. For small account balances, these fees can represent a significant percentage of your investment, potentially eating into returns.

Limited Investment Control: Users can’t pick individual stocks or customize their portfolios beyond choosing a risk level, which may frustrate experienced investors.

Small Returns on Small Balances: Round-ups generate modest amounts—typically $5-$30 monthly for average spenders—meaning it takes time to accumulate meaningful investments.

Market Risk: Like all investments, Acorns portfolios fluctuate with market conditions. Your balance can decrease during downturns, which may be unsettling for new investors.

Better Alternatives for Large Investors: Those with substantial capital may find better value with traditional brokerages offering commission-free trading without subscription fees.

Bottom Line

Acorns excels for investing beginners who want a hands-off approach to building wealth and struggle to save consistently. The round-up feature makes investing invisible and automatic. However, users with larger investment goals or those seeking more control should consider whether the subscription fees justify the convenience, especially when free investment platforms exist.

Qapital App – Gamified Savings Rules & Visual Goal Tracking

- Qapital: Makes saving fun with “savings rules” and visual goal setting for a gamified saving experience.

Qapital transforms saving money into an engaging experience through customizable “savings rules” and visual goal-setting features. This gamification approach makes building financial habits feel less like a chore and more like an achievement.

Pros of Qapital

Customizable Savings Rules: Qapital offers numerous creative automation options—save $5 every time your favorite team wins, round up purchases, or set aside money when you skip your morning coffee. These personalized triggers make saving feel natural and fun.

Visual Goal Tracking: The app displays your progress with images and progress bars for each savings goal, whether it’s a vacation, new laptop, or an emergency fund. This visual motivation keeps you engaged and focused.

Gamified Experience: Earning badges, celebrating milestones, and watching goals fill up taps into reward psychology, making saving money genuinely enjoyable rather than restrictive.

Multiple Goals Simultaneously: Unlike traditional savings accounts, you can work toward several goals at once with clear separation and tracking for each objective.

IFTTT-Style Automation: Tech-savvy users appreciate the “If This, Then That” logic, creating sophisticated savings strategies that align with their lifestyle and spending patterns.

Cons of Qapital

Subscription Fees Required: Most useful features require a $3-$12 monthly subscription. For small savers, these fees can significantly impact actual savings, especially in the early months.

Complexity Can Overwhelm: Too many savings rules running simultaneously might drain your checking account faster than expected, potentially causing cash flow issues or overdrafts.

Not a High-Yield Account: Qapital’s interest rates on savings goals may not be as competitive as dedicated high-yield savings accounts, meaning your money earns less while sitting there.

Requires Discipline: The gamification only works if you engage with it. Users who don’t regularly check progress or adjust rules may find the features underutilized.

Learning Curve: Setting up effective savings rules takes time and experimentation. New users might need several weeks to find the right balance that works for their finances.

Limited Investment Options: While Qapital offers some investing features, it’s primarily a savings app—serious investors will need additional platforms for comprehensive portfolio management.

Bottom Line

Qapital is ideal for individuals who struggle with traditional saving methods and respond well to gamification and visual motivation. The creative savings rules make automation feel personalised rather than restrictive. However, users should ensure subscription costs don’t outweigh their savings progress, and those seeking maximum interest earnings might prefer dedicated high-yield accounts.

Best for: Visual learners, goal-oriented savers, people motivated by gamification, and those who want creative control over their automated savings strategy.

Neobanks and Digital Banking with Integrated Saving Tools

Chime App – Fee-Free Banking with Automatic Savings Tools

- Chime: Offers fee-free banking with automatic savings features from direct deposits and debit card round-ups.

Chime is a mobile-first neobank offering fee-free checking and savings accounts with built-in automation features. By eliminating traditional bank fees and incorporating round-up savings and direct deposit allocations, Chime helps users keep more money while building financial cushions effortlessly.

Pros of Chime

No Monthly Fees: Zero maintenance fees, minimum balance requirements, or overdraft fees (with SpotMe). This saves users an average of $300+ annually compared to traditional banks that charge $12-15 monthly fees.

Automatic Savings Features: Chime’s “Save When You Get Paid” automatically transfers a percentage of direct deposits to savings, and “Round Up” saves spare change from debit purchases—building emergency funds without conscious effort.

Early Direct Deposit: Get your paycheck up to 2 days early when you set up direct deposit, providing crucial cash flow advantages for those living paycheck-to-paycheck.

Large Fee-Free ATM Network: Access 60,000+ fee-free ATMs through MoneyPass and Allpoint networks nationwide, rivaling or exceeding traditional bank ATM accessibility.

SpotMe Overdraft Protection: Qualified users can overdraft up to $200 on debit purchases without fees—a game-changer compared to $35 overdraft charges at traditional banks.

High-Yield Savings: Chime’s savings account offers competitive interest rates (often 2%+) significantly higher than traditional banks’ near-zero rates, helping your money grow faster.

No Foreign Transaction Fees: Use your Chime debit card internationally without extra charges, making it traveler-friendly compared to most traditional debit cards.

Instant Transaction Notifications: Real-time purchase alerts help you track spending and catch fraudulent activity immediately, enhancing security and budgeting awareness.

User-Friendly Mobile App: Intuitive interface makes mobile banking, transfers, and savings management straightforward for tech-savvy users and beginners alike.

Cons of Chime

No Physical Branches: As an online-only bank, you cannot walk into a branch for face-to-face assistance, cash deposits, or complex banking needs—problematic for those preferring in-person service.

Limited Cash Deposit Options: Depositing cash requires visiting retail partners (Walgreens, CVS, 7-Eleven) with associated fees, making cash handling inconvenient and costly compared to traditional banks.

No Joint Accounts: Chime doesn’t offer joint checking accounts, forcing couples or families to use workarounds or maintain separate accounts, complicating shared finances.

Basic Features Only: No checks, money orders, wire transfers, or safe deposit boxes. Users needing these traditional banking services must maintain relationships with conventional banks.

Customer Service Limitations: Support is primarily chat and email-based with no phone number. Users report frustrating wait times and difficulty resolving complex issues without speaking to representatives.

Savings Interest Variable: While currently competitive, Chime’s savings rate fluctuates with market conditions and isn’t guaranteed, potentially dropping below dedicated high-yield savings accounts.

Direct Deposit Required for Best Features: SpotMe overdraft protection and early paycheck access require regular direct deposits, excluding freelancers, gig workers, or those with irregular income.

Account Closure Issues: Some users report sudden account closures or restrictions without clear explanations, leaving them temporarily without access to funds—a serious risk for sole banking relationships.

Limited Bill Pay Options: While you can pay bills, the process is less robust than traditional banks, and some payees may not be supported or experience payment delays.

No Credit Building Products: Chime offers a secured credit card but lacks traditional credit cards, personal loans, or mortgages, limiting comprehensive financial relationship building.

Potential for Overspending: The ease of SpotMe overdraft protection might encourage spending beyond your means, creating a cycle of starting each pay period in the negative.

Bottom Line

Chime excels for digitally-savvy users tired of bank fees and seeking automated savings tools without effort. The fee-free structure and early direct deposit provide real financial advantages, especially for younger users or those with straightforward banking needs. However, it cannot fully replace traditional banks for users requiring physical branches, cash deposits, joint accounts, or comprehensive financial services.

Best for: Younger adults comfortable with mobile-only banking, people paying excessive traditional bank fees, direct deposit recipients wanting early paychecks, users needing SpotMe overdraft protection, and those wanting effortless automatic savings.

Consider alternatives if: You frequently deposit cash, need in-person banking assistance, require joint accounts or business banking, prefer phone customer support, use checks regularly, or want a full-service financial institution.

Smart strategy: Use Chime as your primary checking account for fee savings and automation benefits while maintaining a traditional bank or credit union account for services Chime cannot provide (cash deposits, notary services, safe deposit boxes).

Safety reminder: Don’t rely solely on SpotMe for financial security. The $200 overdraft protection should be an emergency backup, not a regular spending extension. Focus on building actual savings through Chime’s automation features to create a genuine financial cushion.

N26 App Review: Mobile-First Banking with Goal-Oriented Spaces

- N26: A mobile-first bank with “Spaces” for goal-oriented saving and instant spending notifications.

N26 is a European-based mobile bank offering sleek, app-only banking with innovative “Spaces” sub-accounts for goal-oriented saving and real-time spending insights. Known for its modern design and international-friendly features, it brings contemporary banking to users seeking digital-first financial management.

Pros of N26

Spaces for Goal Saving: Create up to 10 separate sub-accounts (Spaces) within your main account for specific goals like vacations, emergency funds, or major purchases. This visual separation makes saving for multiple objectives intuitive and organized.

Instant Transaction Notifications: Every purchase triggers an immediate push notification with merchant details, amount, and remaining balance—providing unmatched spending awareness and fraud detection in real-time.

Sleek Mobile Interface: N26’s beautifully designed app offers intuitive navigation, spending analytics, and financial insights that make banking feel modern rather than bureaucratic.

No Foreign Transaction Fees: Use your N26 card internationally without currency conversion fees on most accounts, making it ideal for frequent travelers or digital nomads.

Quick Account Opening: Open an account entirely through the app in minutes using video identification—no branch visits, paperwork, or lengthy approval processes.

Automatic Categorization: Transactions automatically sort into spending categories (groceries, entertainment, transport) with visual breakdowns showing where money goes each month.

Instant Money Transfers: Send money to other N26 users instantly within the app, and standard SEPA transfers complete faster than traditional banks.

MoneyBeam Feature: Split bills or send money to contacts through a unique QR code system, making peer-to-peer payments quick and seamless.

Premium Card Options: Higher-tier accounts offer premium debit cards (metal cards), travel insurance, and extended ATM withdrawal allowances for users wanting elevated features.

Cons of N26

Limited Geographic Availability: N26 primarily serves European markets. U.S. operations were discontinued in 2022, making it unavailable for American users despite previous expansion attempts.

ATM Withdrawal Limits: Free accounts include only 3-5 free ATM withdrawals monthly depending on your country. Additional withdrawals incur €2+ fees, problematic for cash-dependent users.

No Physical Branches: As a mobile-only bank, there’s no in-person support for complex issues, cash deposits, or services requiring face-to-face interaction.

Basic Savings Interest: N26 Spaces don’t offer competitive interest rates. Your money sits in sub-accounts earning minimal returns compared to dedicated high-yield savings accounts.

Customer Service Challenges: Users report slow response times through chat support, difficulty reaching human agents for urgent issues, and frustration resolving disputes without phone support.

Account Security Concerns: Some users experienced unauthorized account access or fraud, with complaints about N26’s response speed and resolution processes during security incidents.

Limited Financial Products: N26 focuses on checking and basic savings. No mortgages, investment accounts, credit cards (in most markets), or comprehensive wealth management services.

Premium Tier Costs: While the free account is genuinely free, accessing best features (unlimited ATM withdrawals, travel insurance, additional Spaces) requires monthly subscriptions of €4.90-€16.90.

Overdraft Limitations: Overdraft facilities are limited or unavailable in many markets, and when offered, require approval with less generous terms than traditional banks.

Cash Deposit Restrictions: Depositing cash is difficult or impossible in most markets, requiring third-party workarounds or maintaining traditional bank relationships for cash handling.

Regulatory Uncertainty: As a relatively new fintech bank, N26 has faced regulatory scrutiny in some markets, including temporary customer acquisition freezes, raising questions about long-term stability.

Bottom Line

N26 delivers exceptional mobile banking for tech-savvy Europeans who prioritize digital experience, international usability, and goal-oriented saving over traditional banking services. The Spaces feature provides powerful psychological motivation for saving, while instant notifications create spending awareness that promotes financial discipline. However, it works best as a complementary account rather than your sole banking relationship.

Best for: European residents comfortable with mobile-only banking, frequent international travelers, digital nomads needing multi-currency functionality, younger users wanting modern banking interfaces, and goal-oriented savers who benefit from visual financial organization.

Consider alternatives if: You live outside N26’s service areas (including the U.S.), frequently withdraw cash, need in-person banking support, want high-yield savings rates, require comprehensive financial products (mortgages, investments), or prefer phone-based customer service.

Smart usage strategy: Use N26 as your primary spending and travel account while maintaining a traditional bank or high-yield savings account for emergency funds, earning competitive interest. The Spaces feature is perfect for short-to-medium-term goals, but long-term savings deserve higher-yielding homes.

International user tip: N26’s no-fee international transactions make it ideal for travellers, but always carry a backup card from a traditional bank in case of technical issues, card damage, or unexpected account restrictions while abroad.

Availability note: As of 2024, N26 is available in most European Economic Area countries but not in the United States. Always verify current availability in your specific country before attempting to open an account.

SoFi App – All-in-One Platform for Investing & Financial Growth

- SoFi: A comprehensive platform encompassing investments, personal loans, and financial planning, designed for wealth growth.

SoFi (Social Finance) is a comprehensive financial services platform offering investing, banking, loans, and financial planning tools under one roof. Designed to help members build wealth across multiple financial needs, it combines modern fintech convenience with traditional financial products for holistic money management.

Pros of SoFi

All-in-One Financial Ecosystem: Access checking, savings, investments (stocks, ETFs, crypto), personal loans, student loan refinancing, credit cards, and financial planning through a single app—eliminating the need for multiple financial relationships.

No Account Fees: SoFi Invest offers commission-free stock and ETF trading with no account minimums or management fees for active investing, making wealth building accessible regardless of starting capital.

Automated Investing Options: SoFi Automated Investing provides professionally managed portfolios based on your risk tolerance and goals, ideal for hands-off investors wanting diversification without active management.

High-Yield Banking: SoFi Checking and Savings accounts offer competitive APYs (often 4%+) with no monthly fees, minimum balances, or overdraft charges—significantly outperforming traditional banks.

Member Benefits & Perks: Exclusive access to financial advisors, career coaching, networking events, rate discounts on loans, and unemployment protection demonstrates SoFi’s commitment beyond basic financial services.

Fractional Shares: Invest in expensive stocks like Amazon or Google with as little as $5 through fractional share purchases, democratizing access to high-priced securities.

Financial Planning Tools: Free access to certified financial planners for one-on-one guidance on budgeting, investing strategy, debt management, and goal setting—typically a paid service elsewhere.

Competitive Loan Rates: SoFi’s personal loans and student loan refinancing often feature lower rates than competitors, especially for borrowers with strong credit profiles.

Cryptocurrency Trading: Buy and sell popular cryptocurrencies directly within the platform alongside traditional investments, offering diversification into digital assets.

Retirement Account Options: Traditional, Roth, and SEP IRAs available with tax advantages for long-term retirement savings alongside standard brokerage accounts.

Cons of SoFi

Limited Investment Research Tools: While adequate for beginners, SoFi’s investment platform lacks the sophisticated research, advanced charting, and analysis tools offered by established brokerages like Fidelity or Schwab.

Loan Eligibility Requirements: SoFi’s competitive loan rates require strong credit scores and income levels. Those with poor credit or limited income may not qualify or receive less favorable terms.

No Physical Branches: As an online-only platform, SoFi offers no in-person service for complex issues, cash deposits, or face-to-face consultations—problematic for those preferring traditional banking.

Automated Investing Fees: While active investing is free, SoFi Automated Investing charges 0.25% annually—reasonable but higher than some robo-advisors like Betterment or Wealthfront at certain account levels.

Limited Investment Options: No mutual funds, bonds, or options trading available. Investors wanting these asset classes must use additional platforms, limiting portfolio diversification strategies.

Customer Service Inconsistency: Users report variable support quality, with some experiencing quick resolutions while others face delayed responses or difficulty reaching knowledgeable representatives for technical issues.

Financial Advisor Limitations: While free advisor access is valuable, sessions are time-limited and advisors cannot execute trades or manage accounts directly—more consultative than comprehensive wealth management.

ATM Fee Reimbursement Caps: SoFi reimburses out-of-network ATM fees but with monthly limits. Frequent cash users may still incur charges beyond reimbursement thresholds.

Loan Origination Fees: Some SoFi loan products include origination fees (0-7%) that reduce net proceeds or increase effective borrowing costs despite advertised competitive rates.

Product Cross-Selling: Users report aggressive marketing for additional SoFi products through email and in-app notifications, which can feel pushy when you’re only interested in specific services.

Less Established Than Traditional Banks: As a newer fintech company (founded 2011), SoFi lacks the decades-long track record of stability that traditional banks offer, creating potential concerns during economic downturns.

Bottom Line

SoFi excels for financially-engaged individuals seeking a streamlined, all-in-one platform for wealth building without juggling multiple financial institutions. The combination of high-yield banking, commission-free investing, competitive loans, and free financial planning creates genuine value, especially for members utilizing multiple products. However, advanced investors or those requiring sophisticated tools should supplement SoFi with specialized platforms.

Best for: Young professionals building wealth, individuals consolidating financial accounts, borrowers with strong credit seeking competitive loan rates, hands-off investors wanting automated portfolios, and financially-engaged users valuing member perks and community.

Consider alternatives if: You need advanced investment research and trading tools, prefer in-person banking services, have poor credit limiting loan access, want access to mutual funds and bonds, require extensive cash deposit capabilities, or prefer specialized best-in-class services over all-in-one convenience.

Wealth-building strategy: Maximize SoFi’s ecosystem by combining high-yield savings for emergency funds, automated investing for retirement accounts, and active investing for individual stock positions. Use free financial planner consultations to optimize your overall strategy across products.

Loan refinancing caution: While SoFi’s student loan refinancing offers competitive rates, carefully evaluate whether refinancing federal loans into private loans sacrifices valuable protections like income-driven repayment plans, forbearance options, or potential forgiveness programs.

Membership maximization tip: SoFi members using multiple products unlock the most value through rate discounts, higher benefits tiers, and integrated financial management. If only using one service, specialized competitors may offer superior features for that specific need.

Current App – Goal-Based Savings Pods & High-Interest Banking

- Current: Provides savings “pods” for specific goals and earns interest rates on deposits, offering a flexible alternative to traditional banking.

Current is a mobile banking app featuring innovative “savings pods” that let users organize money into specific goal categories while earning competitive interest rates. Designed as a flexible alternative to traditional banking, it combines modern financial management tools with fee-free accounts for everyday banking needs.

Pros of Current

Savings Pods for Goal Organization: Create up to three customizable savings pods (or more with premium) for specific objectives like emergency funds, vacation savings, or holiday shopping. This visual separation provides psychological clarity and motivation for multiple financial goals.

Competitive Interest Rates: Current offers interest on both checking balances and savings pods, with rates often exceeding 4% APY—dramatically outperforming traditional banks’ near-zero rates and helping your money grow faster.

Faster Direct Deposits: Get your paycheck up to 2 days early with direct deposit, providing crucial cash flow advantages for those managing tight budgets or living paycheck-to-paycheck.

No Overdraft Fees: Current’s Overdrive feature allows eligible users to overdraft up to $200 without fees, eliminating the $35 penalties that traditional banks charge for insufficient funds.

Fee-Free Banking: No monthly maintenance fees, minimum balance requirements, or hidden charges. Access 40,000+ fee-free ATMs through the Allpoint network nationwide.

Instant Gas Hold Release: Unlike traditional banks that place multi-day holds on gas station purchases, Current releases these holds within hours, keeping your available balance accurate.

Spending Insights & Notifications: Real-time transaction alerts and automatic spending categorization help you track where money goes and catch fraudulent activity immediately.

Teen Accounts Available: Parents can open Current accounts for teens (13+) with parental controls, spending limits, and real-time monitoring—teaching financial responsibility while maintaining oversight.

Round-Up Savings: Automatically round debit purchases to the nearest dollar and transfer spare change to savings pods, building funds painlessly through everyday spending.

Cash-Back Rewards: Earn points on debit card purchases at participating merchants, redeemable for cash or gift cards, adding value to everyday transactions.

Cons of Current

Premium Tier Required for Best Features: While the free account works, accessing multiple savings pods, highest interest rates, and enhanced overdraft protection requires Current Premium at $4.99-$9.99 monthly.

Limited Pod Numbers on Free Plan: Free users can only create 1-3 savings pods depending on account tier, restricting goal organization flexibility compared to unlimited sub-accounts at some competitors.

Interest Rate Variability: Current’s APY fluctuates with market conditions and isn’t guaranteed. Rates can drop below dedicated high-yield savings accounts from traditional online banks.

No Physical Branches: As a mobile-only bank, there’s no in-person support for complex issues, cash deposits, or services requiring face-to-face interaction with banking staff.

Cash Deposit Limitations: Depositing cash requires visiting retail partners (CVS, Rite Aid, 7-Eleven) with fees up to $3.50 per deposit, making cash handling expensive and inconvenient.

Customer Service Challenges: Users report inconsistent support quality, slow response times through chat-only channels, and difficulty resolving account issues without phone support options.

Basic Banking Features Only: No checks, wire transfers, cashier’s checks, or safe deposit boxes. Users needing traditional banking services must maintain relationships with conventional banks.

Overdrive Eligibility Requirements: The $200 overdraft feature requires qualifying direct deposits of $500+ monthly, excluding gig workers, freelancers, or those with irregular income from this benefit.

Account Closure Concerns: Some users report unexpected account freezes or closures without clear explanations, temporarily blocking access to funds—a serious risk for sole banking relationships.

Limited Bill Pay Options: While basic bill payment exists, the functionality is less robust than traditional banks, and some payees may not be supported or experience payment delays.

ATM Withdrawal Limits: Even premium accounts have daily ATM withdrawal limits that may be restrictive for users needing large cash amounts for legitimate purposes.

Interest Paid on Limited Balances: Some interest rate promotions apply only to balances up to certain thresholds (e.g., first $6,000), with lower rates on amounts exceeding caps.

Bottom Line

Current works well for digitally-savvy users seeking visual goal organization through savings pods combined with competitive interest rates and early paycheck access. The fee-free structure and overdraft protection provide genuine advantages over traditional banks, especially for younger users or those with straightforward banking needs. However, premium costs and limitations make it best suited as a complement to rather than replacement for comprehensive banking relationships.

Best for: Goal-oriented savers who benefit from visual money separation, younger adults comfortable with mobile-only banking, direct deposit recipients wanting early access, parents seeking teen banking solutions with oversight, and users paying excessive traditional bank fees.

Consider alternatives if: You frequently deposit cash, need in-person banking assistance, want unlimited savings goal categories on free accounts, require traditional banking products (checks, wire transfers), prefer phone customer support, or need consistently highest savings rates.

Optimization strategy: Use Current’s free tier for basic checking and 1-3 primary savings goals while maintaining a dedicated high-yield savings account elsewhere for long-term emergency funds earning guaranteed competitive rates. Only upgrade to premium if you’ll fully utilize additional pods and enhanced features.

Teen banking advantage: Current’s teen accounts with parental controls offer exceptional financial education opportunities. Parents can monitor spending, set limits, and teach budgeting in real-world scenarios while maintaining safety guardrails.

Interest rate reality check: While Current’s rates are competitive today, always compare against dedicated high-yield savings accounts from Ally, Marcus, or American Express, which may offer higher guaranteed rates without premium subscriptions. Current’s all-in-one convenience may justify slightly lower rates for some users.

Advanced Budgeting and Expense Management Apps

Mint App – Complete Financial Overview & Budget Management

- Mint: Aggregates financial data, offers real-time spending tracking, and personalised budgeting tips across multiple accounts.

Mint is a comprehensive financial management app that aggregates all your accounts in one place, providing real-time spending tracking and personalized budgeting insights. As one of the most established personal finance apps, it offers a complete financial dashboard at no cost.

Pros of Mint

Complete Financial Snapshot: Mint connects to bank accounts, credit cards, loans, and investments, giving you a unified view of your entire financial life. This eliminates the need to log into multiple accounts to check balances.

Real-Time Spending Tracking: Transactions automatically categorize as they occur, helping you understand where your money goes without manual entry. This instant visibility prevents overspending surprises at month’s end.

Personalized Budgeting Tools: Mint analyzes your spending patterns and suggests realistic budget categories based on your actual behavior, making budgets easier to stick to than arbitrary limits.

Free to Use: Unlike many competitors, Mint offers its core features completely free, making professional-grade financial management accessible to everyone regardless of income level.

Bill Reminders & Alerts: The app notifies you about upcoming bills, unusual spending, low balances, and potential fees, helping you avoid costly mistakes.

Credit Score Monitoring: Mint provides free credit score tracking and insights into factors affecting your creditworthiness, typically a paid feature elsewhere.

Historical Data & Trends: View spending trends over time to identify patterns, seasonal expenses, and areas for improvement in your financial habits.

Cons of Mint

Ad-Supported Model: Since Mint is free, it generates revenue through financial product recommendations and ads, which some users find intrusive or distracting.

Limited Customization: Budget categories and transaction categorization can be rigid. Users wanting highly customized systems may find Mint’s structure restrictive.

Automatic Categorization Errors: Mint sometimes miscategorizes transactions, requiring manual corrections that can be tedious for those with high transaction volumes.

Read-Only Access: You can view financial data but cannot initiate transfers or payments within Mint, requiring you to log into individual bank apps for transactions.

Privacy Concerns: Aggregating all financial data in one platform creates a single point of vulnerability. While Mint uses bank-level security, some users are uncomfortable with third-party access to all accounts.

Intuit Shutdown Announced: Intuit discontinued Mint in early 2024, migrating users to Credit Karma. Existing Mint users should verify current availability and consider alternatives.

No Investment Management: While Mint tracks investment accounts, it doesn’t offer portfolio analysis, rebalancing suggestions, or investment management tools.

Customer Support Limitations: As a free service, Mint’s customer support can be slow or limited compared to paid financial services.

Bottom Line

Mint excels as a comprehensive, free budgeting tool for users who want complete financial visibility without paying subscription fees. The automatic tracking and aggregation save significant time compared to manual budgeting methods. However, users should note the service’s transition status and weigh privacy considerations against the convenience of centralised financial data.

Best for: Budget-conscious individuals, people managing multiple accounts, those new to budgeting who need guidance, and users comfortable with ad-supported free services.

Note: As of 2024, Mint has been discontinued by Intuit. Users should explore alternatives like Credit Karma (Intuit’s replacement), YNAB, or Copilot for similar functionality. Intuit, Mint’s owner, encouraged users to move to Credit Karma, which offers some basic features like spending categorisation, but lacks Mint’s robust budgeting tools.

Rocket Money – Subscription Tracker & Bill Negotiation Service

- Rocket Money (formerly Truebill): Specializes in subscription management, expense tracking, and bill negotiation to reduce unnecessary spending.

Rocket Money (formerly Truebill) is a financial app that identifies and cancels unwanted subscriptions, tracks expenses, and negotiates bills on your behalf to lower monthly costs. It’s designed to help users reclaim money lost to forgotten subscriptions and overpriced services.

Pros of Rocket Money

Subscription Discovery & Cancellation: Rocket Money scans your accounts to find all active subscriptions, including forgotten streaming services, trial periods that auto-renewed, and recurring charges you no longer use. You can cancel directly through the app without navigating multiple websites.

Bill Negotiation Service: The app’s concierge team negotiates with service providers (cable, internet, phone) to lower your bills. They handle the entire process, often securing discounts of 10-30% without you making a single call.

Spending Insights: Automated expense tracking categorizes purchases and identifies spending patterns, helping you understand where money disappears each month beyond just subscriptions.

Smart Savings Features: Rocket Money can automatically transfer small amounts to savings based on your spending habits and account balance, building emergency funds painlessly.

Custom Budget Alerts: Set spending limits by category and receive notifications when approaching or exceeding budgets, preventing overspending in real-time.

Net Worth Tracking: Monitor assets and liabilities in one dashboard, providing a complete picture of your financial health over time.

Refund Recovery: The app identifies potential refunds from overcharges, duplicate transactions, or subscription billing errors.

Cons of Rocket Money

Premium Pricing: While there’s a free tier, most valuable features (bill negotiation, smart savings, custom budgets) require a premium subscription starting at $6-12 monthly, with flexible pricing that some find confusing.

Success Fees on Negotiations: When Rocket Money successfully negotiates bills, they may charge 30-60% of the first year’s savings—which can add up if they secure significant discounts.

Limited Free Features: The free version is quite restricted, essentially serving as a trial to encourage premium upgrades. Serious users will likely need to pay.

Bill Negotiation Results Vary: Success depends on your provider and location. Some users report minimal savings or no success, meaning you pay subscription fees without guaranteed results.

Privacy Trade-Offs: Like all financial aggregators, Rocket Money requires access to your banking data. While secure, this centralization makes some users uncomfortable.

Aggressive Upselling: Free users report frequent prompts to upgrade, which can feel pushy when you’re trying to navigate the app.

Manual Subscription Input: Some subscriptions charged to PayPal, Venmo, or prepaid annually may not auto-detect, requiring manual tracking.

Customer Service Issues: Some users report difficulty cancelling Rocket Money’s own subscription or delays in customer support responses—ironic for a subscription management service.

Bottom Line

Rocket Money shines for people with multiple subscriptions they’ve lost track of and those paying high bills for cable, internet, or phone services. The bill negotiation feature can pay for itself if successful, potentially saving hundreds annually. However, users with few subscriptions or already-optimized bills may not find enough value to justify the premium cost.

Best for: Subscription-heavy users, people overwhelmed by recurring charges, those with negotiable bills (cable/internet/phone), and individuals who hate confrontational customer service calls.

Consider alternatives if: You have few subscriptions, prefer completely free tools, or want more comprehensive budgeting features alongside subscription management.

Money-saving tip: Even one month of Rocket Money Premium can help you identify and cancel forgotten subscriptions, potentially saving more than the subscription cost long-term.

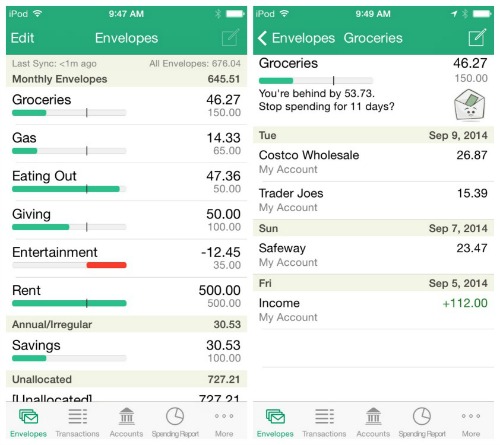

Goodbudget App – Digital Envelope Budgeting & Family Finance

- Goodbudget: A digital adaptation of the “envelope budgeting method,” allowing manual input and family sharing for hands-on control.

Goodbudget brings the traditional envelope budgeting method into the digital age, allowing users to manually allocate funds into virtual “envelopes” for different spending categories. With family sharing capabilities, it’s designed for hands-on budgeters who want intentional control over their money.

Pros of Goodbudget

Proven Envelope Method: Based on a time-tested cash envelope system, Goodbudget helps you allocate every dollar to specific purposes (groceries, entertainment, bills), preventing overspending and promoting intentional money decisions.

Manual Transaction Entry: Unlike automatic syncing apps, manual input forces you to consciously engage with every purchase, increasing financial awareness and accountability—a powerful behavior change tool.

Family Sync Capability: Multiple users can access the same budget in real-time, making it ideal for couples or families managing shared finances. Everyone sees updated envelope balances instantly after purchases.

No Bank Account Linking Required: For privacy-conscious users, Goodbudget doesn’t require bank credentials or access to your accounts, eliminating security concerns associated with account aggregation.

Debt Tracking Features: Built-in debt payoff tools help you visualize and strategize paying down loans and credit cards using proven methods like debt snowball or avalanche.

Reports & Insights: Historical spending reports show trends across envelopes, helping identify problem areas and celebrate progress over time.

Free Version Available: The basic plan offers limited envelopes at no cost, allowing users to test the methodology before committing financially.

Cross-Platform Access: Works on web, iOS, and Android, so you can update budgets from any device wherever you are.

Cons of Goodbudget

Manual Entry Time Commitment: Logging every transaction requires discipline and time. Busy users or those with high transaction volumes may find this tedious and eventually abandon the system.

No Automatic Syncing: Unlike competitors, Goodbudget won’t automatically import bank transactions, meaning you must manually record everything or risk inaccurate budgets.

Limited Free Version: The free plan restricts you to 20 envelopes and one account, which may be insufficient for complex household budgets or families tracking multiple income sources.

Envelope Limits on Paid Plans: Even premium versions cap envelope numbers (though at higher limits), which could frustrate users wanting granular category breakdowns.

Steeper Learning Curve: The envelope concept isn’t intuitive for everyone. Users unfamiliar with this budgeting philosophy may need time to understand and implement it effectively.

No Bill Pay Integration: You can track bills in envelopes but cannot pay them directly through the app, requiring separate logins to actual bank or service provider accounts.

Potential for User Error: Manual entry means typos, forgotten transactions, or incorrect amounts can throw off your entire budget without automatic reconciliation against bank statements.

Basic Interface Design: Compared to modern fintech apps, Goodbudget’s interface feels dated and less visually engaging, which may not appeal to users wanting sleek, intuitive designs.

Bottom Line

Goodbudget is perfect for intentional budgeters who value hands-on financial control and want to deeply understand their spending habits. The manual entry requirement—though time-consuming—creates powerful awareness that automatic apps can’t replicate. It’s especially valuable for couples and families needing synchronized budget visibility without sharing bank credentials.

Best for: Envelope budgeting enthusiasts, couples managing joint finances, privacy-focused users avoiding bank linking, people who benefit from manual transaction awareness, and families teaching children budgeting fundamentals.

Consider alternatives if: You want automated tracking, have extremely high transaction volumes, prefer set-it-and-forget-it systems, or need advanced investment tracking and bill pay features.

Success tip: Commit to logging transactions immediately after purchases (or daily at a minimum) to maintain accuracy and prevent the system from becoming overwhelming.

Simplified Investment Platforms for Entry-Level Investors

Robinhood App – Commission-Free Trading for Beginner Investors

- Robinhood: Popular for commission-free trading of stocks, ETFs, and cryptocurrencies, lowering entry barriers for beginners.

Robinhood revolutionized investing by offering commission-free trading of stocks, ETFs, options, and cryptocurrencies with no account minimums. Its simple interface and accessible approach have made it the go-to platform for first-time investors entering the market.

Pros of Robinhood

Zero Commission Trading: Buy and sell stocks, ETFs, options, and cryptocurrencies without paying per-trade fees that traditional brokers charge. This makes frequent trading and small investments financially viable.

No Account Minimums: Start investing with any amount—even $1. Fractional shares let you buy portions of expensive stocks like Amazon or Tesla, removing the barrier of needing thousands to build a diversified portfolio.

User-Friendly Interface: The clean, intuitive app design makes investing approachable for beginners. Clear visuals, simple navigation, and straightforward buying/selling processes reduce intimidation for new investors.

Cryptocurrency Access: Trade popular cryptocurrencies like Bitcoin, Ethereum, and Dogecoin alongside traditional stocks in one platform, offering diversification beyond conventional markets.

Instant Deposits: Access funds immediately after transferring from your bank (up to limits) rather than waiting days, allowing you to capitalize on market opportunities quickly.

Extended Trading Hours: Trade during pre-market and after-hours sessions, giving you flexibility beyond standard 9:30 AM – 4:00 PM market hours.

Cash Management Features: Robinhood offers a cash card and spending account with competitive interest rates, combining investing and everyday banking.

Real-Time Market Data: Free access to live price updates and basic charts without requiring premium subscriptions like some competitors charge.

Cons of Robinhood

Limited Research Tools: Robinhood provides minimal fundamental analysis, company research, or educational resources compared to established brokers like Fidelity or Schwab. Beginners may make uninformed decisions.

Encourages Risky Behavior: The gamified interface with confetti animations and push notifications can encourage impulsive, emotion-driven trading rather than long-term investing strategies.

Customer Service Issues: Users report difficult-to-reach support, slow response times, and lack of phone assistance during critical trading issues or account problems.

Payment for Order Flow Controversy: Robinhood profits by selling order flow to market makers, which critics argue may result in less favorable trade execution prices despite “free” trades.

Limited Account Types: No joint accounts, custodial accounts for minors, or trust accounts. IRA options exist but are more limited than traditional brokers.

Trading Restrictions History: During the 2021 GameStop controversy, Robinhood restricted trading on certain volatile stocks, frustrating users and raising questions about platform reliability during market stress.

Basic Tax Reporting: Tax documents can be confusing for active traders, and the platform offers limited tax-loss harvesting or optimization tools available elsewhere.

No Mutual Funds: Robinhood doesn’t offer mutual funds, limiting diversification options for investors who prefer these professionally managed products.

Cryptocurrency Limitations: You cannot transfer cryptocurrencies to external wallets (though this feature is gradually rolling out), meaning you don’t truly “own” your crypto in the traditional sense.

Bottom Line

Robinhood excels at lowering barriers for beginner investors through commission-free trading, fractional shares, and an approachable interface. It’s ideal for those making their first investments or building portfolios with limited capital. However, serious investors seeking comprehensive research, advanced tools, or hands-on customer support should consider more established brokerages.

Best for: First-time investors, young adults starting small, casual traders comfortable with self-directed research, and users wanting cryptocurrency and stock access in one simple app.

Consider alternatives if: You need robust research tools, prefer human financial advisors, want comprehensive retirement account options, require responsive customer service, or plan sophisticated trading strategies.

Investing reminder: Commission-free trading doesn’t mean risk-free investing. The ease of trading on Robinhood can encourage overtrading, which typically reduces returns. Focus on long-term strategies rather than chasing short-term market movements.

Coinbase App – Secure Cryptocurrency Trading & Wallet Storage

- Coinbase: A secure and user-friendly platform for cryptocurrency trading and storage, known for robust security protocols.

Coinbase is one of the largest and most trusted cryptocurrency exchanges, offering a beginner-friendly platform for buying, selling, and storing digital assets like Bitcoin, Ethereum, and thousands of altcoins. Known for robust security measures and regulatory compliance, it’s become the default entry point for crypto newcomers.

Pros of Coinbase

Industry-Leading Security: Coinbase stores 98% of customer funds in offline cold storage, uses two-factor authentication, biometric logins, and insurance coverage for digital assets held online—providing peace of mind in the often-risky crypto space.

Beginner-Friendly Interface: The intuitive design makes cryptocurrency accessible to first-timers. Clear buying processes, educational tooltips, and straightforward navigation remove the technical intimidation factor associated with crypto investing.

Regulatory Compliance: As a publicly-traded U.S. company, Coinbase adheres to strict financial regulations, anti-money laundering rules, and tax reporting requirements, offering legitimacy that many exchanges lack.

Wide Cryptocurrency Selection: Access hundreds of cryptocurrencies beyond just Bitcoin and Ethereum, allowing diversification across the crypto ecosystem from established coins to emerging projects.

Educational Rewards Program: “Coinbase Earn” pays you in cryptocurrency for watching educational videos and completing quizzes about different coins—a unique way to learn while building a small portfolio.

Multiple Product Tiers: Coinbase offers a basic app for beginners and Coinbase Advanced (formerly Pro) for experienced traders wanting sophisticated charting tools and lower fees.

Staking Opportunities: Earn passive income by staking supported cryptocurrencies directly through the platform, with rewards automatically deposited to your account.

Wallet Control: Unlike some exchanges, Coinbase allows you to transfer cryptocurrencies to external wallets, giving you true ownership and control over your digital assets.

Bank Integration: Easy ACH transfers, debit card purchases, and PayPal connectivity make funding your account straightforward compared to more technical exchanges.

Cons of Coinbase

High Fees for Beginners: The standard Coinbase app charges significant fees (often 1-3% plus spread) on transactions. These costs eat into profits, especially for small purchases or frequent traders.

Coinbase Advanced Learning Curve: While the basic app is user-friendly, accessing lower fees requires using Coinbase Advanced, which has a steeper learning curve that defeats the simplicity advantage.

Limited Customer Support: Users frequently report slow response times, difficulty reaching human support, and frustrating resolution processes for account issues or locked funds.

Account Restrictions: Some users experience sudden account limitations, identity verification problems, or trading restrictions without clear explanations, causing significant inconvenience.

Not Your Keys Initially: While you can transfer crypto out, assets held on Coinbase are technically in the exchange’s custody until moved to a personal wallet—creating potential vulnerability.

Geographic Limitations: Not all features and cryptocurrencies are available in every country or U.S. state due to varying regulations, limiting accessibility for some users.

Price Slippage: The spread (difference between buy and sell prices) can be wider than competitor exchanges, meaning you pay more when buying and receive less when selling.

Taxable Events Complexity: Every crypto-to-crypto trade, sale, or spending creates a taxable event. Coinbase provides tax documents, but complex trading histories can create accounting nightmares.

Centralization Risks: As a centralized exchange, Coinbase is vulnerable to hacks, regulatory seizures, or operational failures, though their security track record has been relatively strong.

Bottom Line

Coinbase is the gold standard for cryptocurrency beginners prioritizing security and ease of use over rock-bottom fees. Its regulatory compliance, educational resources, and intuitive interface make crypto investing accessible to mainstream users hesitant about the space. However, active traders and cost-conscious investors should explore Coinbase Advanced or alternative exchanges with lower fee structures.

Best for: Crypto beginners, security-conscious investors, users wanting regulatory compliance and insurance protection, people interested in earning while learning, and those prioritizing user experience over minimal fees.

Consider alternatives if: You’re an experienced trader seeking the lowest possible fees, need advanced technical analysis tools, want decentralized exchange benefits, or trade high volumes where fee percentages significantly impact returns.

Crypto safety reminder: Even on secure platforms like Coinbase, enable all security features (2FA, biometric login, withdrawal whitelisting), never share account credentials, and consider transferring significant holdings to a personal hardware wallet for maximum security. Remember that cryptocurrency markets are highly volatile and speculative—only invest what you can afford to lose.

Cashback and Rewards for Passive Saving

Upside App – Cash-Back Rewards on Gas, Groceries & Dining

- Upside (formerly GetUpside): Provides cash-back rewards on everyday purchases like fuel and groceries, turning spending into savings.

Upside (formerly GetUpside) is a cash-back rewards app that offers instant savings on everyday purchases at gas stations, grocery stores, and restaurants. By partnering with local businesses, it turns routine spending into measurable savings without requiring credit cards or loyalty program juggling.

Pros of Upside

Significant Gas Savings: Earn up to 25¢ per gallon cash back on fuel purchases—one of the highest rates available. For frequent drivers, this translates to hundreds of dollars annually in recovered spending.

No Credit Card Required: Unlike traditional cash-back credit cards, Upside works with any payment method (debit cards, credit cards, even cash). Simply claim offers before purchasing and submit receipt photos afterward.

Everyday Essential Categories: Beyond gas, earn cash back on groceries and restaurant meals—purchases you’re already making. This transforms unavoidable spending into recovered money.

Stackable Rewards: Upside cash back stacks with credit card rewards and store loyalty programs, maximizing total savings on each transaction rather than choosing one program.

Easy Cash-Out Options: Redeem earnings through direct bank transfer, PayPal, or gift cards with low minimum thresholds ($10-15), making rewards accessible quickly.

Location-Based Offers: The app shows nearby participating businesses with available cash-back percentages, helping you choose where to shop strategically based on savings potential.

No Points Complexity: Earn straightforward cash, not complicated points systems requiring conversion calculations or expiration tracking.

Free to Use: No subscription fees, membership costs, or premium tiers—the app generates revenue through business partnerships, not user charges.

Cons of Upside

Limited Participating Locations: Availability varies significantly by region. Rural areas or certain cities may have few participating gas stations, grocery stores, or restaurants, limiting usefulness.

Must Claim Offers First: You cannot earn retroactive cash back. You must open the app, claim an offer, and shop within the specified timeframe—forgetting this step means no rewards.

Receipt Submission Required: After purchases, you must photograph and upload receipts for verification. This extra step feels tedious compared to automatic credit card cash-back programs.

Lower Rates Than Advertised: The headline “up to 25¢ per gallon” rates are maximums. Actual offers often range 5-15¢ per gallon depending on location, time, and competition—still valuable but less impressive.

Processing Delays: Cash-back doesn’t appear instantly. Verification takes 4-24 hours, and first-time users may wait longer, creating uncertainty about whether submissions succeeded.

Potential for Inconvenience: Chasing the highest cash-back rate might send you to less convenient locations, wasting time and fuel that offsets savings—especially if the station is out of your way.

Data Privacy Considerations: Upside tracks your location and purchase behavior to serve relevant offers. Privacy-conscious users may be uncomfortable with this level of data collection.

Receipt Photo Quality Issues: Rejected submissions due to blurry photos, missing information, or faded receipts create frustration and lost rewards, requiring resubmission efforts.

Gas Quality Concerns: Some participating stations are lesser-known brands. Users report occasional concerns about fuel quality at certain locations offering the highest cash-back rates.

Limited Customer Support: Users report difficulty resolving disputed transactions, missing cash back, or technical issues through customer service channels.

Bottom Line

Upside delivers genuine value for people who drive regularly and shop at participating locations along their normal routes. The gas savings alone can justify using the app, especially for commuters or road-trippers. However, it requires active engagement—claiming offers and photographing receipts—making it less passive than credit card rewards but potentially more lucrative for specific categories.

Best for: Frequent drivers, commuters with flexible gas station choices, budget-conscious shoppers who don’t mind extra steps for savings, people without cash-back credit cards, and families with high fuel and grocery expenses.

Consider alternatives if: You have few participating locations nearby, prefer completely passive cash-back systems, find receipt submission too tedious, already maximize credit card rewards, or value convenience over optimized savings.

Maximizing savings tip: Check Upside before every gas fill-up to make it a habit. Even 10¢ per gallon on a 12-gallon tank saves $1.20 per fill-up—$60+ annually for weekly fill-ups. Combine with a cash-back credit card for double rewards on the same purchase.

Reality check: While Upside provides real savings, don’t drive significantly out of your way for marginally better rates. Calculate whether the detour costs more in time, fuel, and vehicle wear than the extra cash back earned.

Crucial Attributes of an Effective FinTech Saving App

When looking for the best FinTech app to support your financial goals, there are several key attributes to consider. It’s not just about flashy features; it’s about reliability and alignment with your personal financial guide.

Paramount Security Measures

**Your** **money** and personal data are invaluable. The **top** **apps** implement robust security, including two-factor authentication (2FA), data encryption, and biometric logins. Always ensure that deposited funds are FDIC-insured via partner institutions for protection up to $250,000. Adherence to regulatory compliance like KYC (Know Your Customer) and AML (Anti-Money Laundering) also protects **your** data and funds.

User-Centric Design and Experience

An effective app should be intuitive. An easy-to-navigate interface helps you quickly comprehend complex financial data. Clear visualization of financial progress and goal attainment, like seeing your savings account grow towards your emergency fund or retirement plan, keeps you motivated.

Transparent Fee Structures

No one likes surprises, especially with money. The best apps have clear disclosure of any service or transaction charges. Many popular options, like Chime and Robinhood (for basic services), are known for their fee-free models. Always understand the cost upfront.

Versatility and Interoperability

The capability to manage diverse financial aspects within a single application, from budgeting to investing, can be a huge convenience. Compatibility with other financial tools and services through integrations further enhances your financial freedom.

Alignment with Personal Financial Objectives

Ultimately, the best app for you is the one that directly addresses your specific needs. Are you focused on debt reduction, wealth accumulation, or daily budgeting tips? I suggest an experiential evaluation of multiple platforms. Find the app that truly fits your way of life and financial plan.

The Future Trajectory of Automated Saving FinTech

The FinTech Market is continuously evolving, and the future of automated saving looks even more intelligent and integrated.

Advanced AI and Machine Learning Integration

We’re already seeing impressive AI, and it’s only going to get better. Expect evolution towards predictive financial analytics and hyper-personalized recommendations, not just for saving, but also for smart investment strategy. Imagine automated adjustments to investment strategies and savings goals based on real-time Market changes and your personal behavior – all without your active input.

Expansion of Blockchain and Decentralized Finance (DeFi)

The integration of cryptocurrency and blockchain technology into mainstream savings and investment products is increasing. This opens up the potential for novel, transparent, and efficient financial ecosystems, potentially offering new ways to save and grow your money.

Pervasive Embedded Finance

Imagine financial services seamlessly integrated directly into non-financial apps and daily activities. This could make saving an inherent part of consumption and lifestyle apps, further reducing the conscious effort needed to bolster your financial health.

Conclusion: Empowering Financial Wellness Through Smart FinTech

FinTech has truly transformed personal finance, making saving more accessible and less daunting than ever before. These apps facilitate effortless saving through automation, intelligent features, and comprehensive financial visibility. My experience shows that by leveraging these tools, you can achieve your financial goals with minimal active management, freeing up your time and reducing stress.

I encourage you to explore and adopt FinTech solutions tailored to your unique financial journey. Leveraging these smart tools is a strategic step towards enhanced financial security and independence. It’s your way to save smarter, not harder, and build a stronger financial future.

Disclaimer

Please note that this blog post is intended for informational purposes only and should not be construed as financial advice. The content provided is based on general information and publicly available data. We are not certified financial planners or advisors. Before making any financial decisions, especially those related to investing, saving, or debt management, we strongly recommend consulting with a qualified and certified financial professional who can provide personalized advice based on your individual circumstances and financial objectives. All links to third-party companies are for informational purposes and convenience only.

References

- C. Frazer and B. Wren, “9 Best Money Saving Apps Of 2025,” Bankrate, Jan. 31, 2025. [Online]. Available: https://www.bankrate.com/personal-finance/best-money-saving-apps/

- Trio, “Top 12 Fintech Apps You Must Check Out in 2025 for Smart Finance,” Trio.dev, Apr. 24, 2025. [Online]. Available: https://trio.dev/fintech-apps-you-must-check-out/

- B. Carlin, A. Olafsson, and M. Pagel, “Mobile Apps and Financial Decision Making,” *Review of Finance*, vol. 27, no. 3, pp. 977–1013, 2023. [Online]. Abstract available: https://business.rice.edu/wisdom/can-mobile-banking-app-really-save-you-money

- J. Koetsier, “Top 100 fintech apps for 2025 – Singular,” Singular, Mar. 17, 2025. [Online]. Available: https://www.singular.net/blog/top-fintech-apps/

Image Credit

analogicushttps://cdn.pixabay.com/user/2022/02/27/22-44-21-106_250x250.jpg