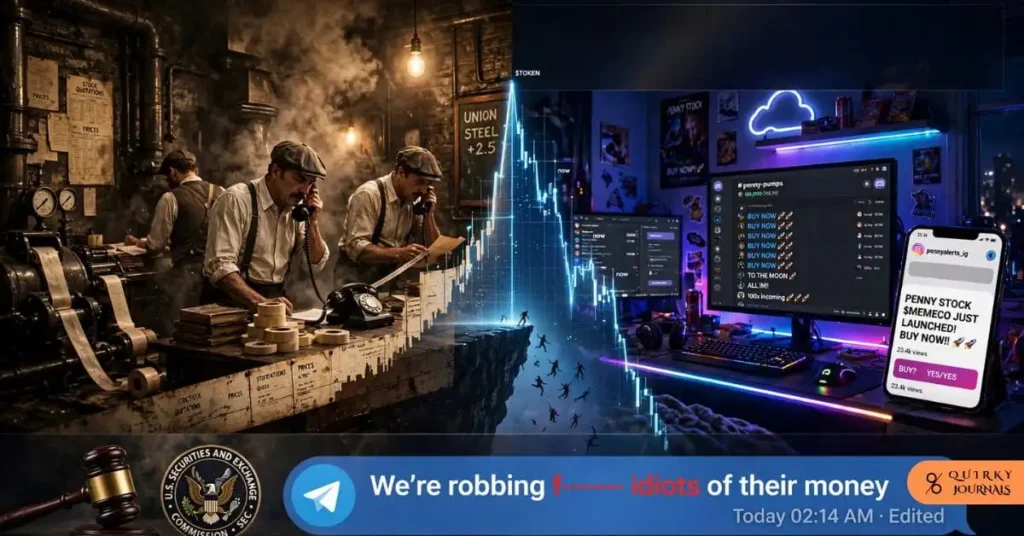

Pump and Dump in the Age of Influencers: How Financial Fraud Moved to Instagram and Discord

Pump and dump is the oldest financial fraud, but Instagram and Discord gave it superpowers. See how influencers like Atlas Trading turned 300K followers into a 20-minute boiler room, why low-liquidity assets are targets, and how the SEC is fighting fraud at internet speed.