College Majors With the Worst Debt: Data on What Actually Pays

Nobody hands you a debt calculator on orientation day. They should. Because the major you pick at 18 can shackle you to a loan payment well into your 40s, and most freshmen have no idea how steep that number can get.

We’re going to walk through the real data. Not vibes, not “follow your passion” platitudes. Actual median debt figures by major and degree level, cross-referenced against what those degrees actually pay once you’re out.

Some of these numbers will surprise you. Others will confirm what you already suspected about that psychology degree your cousin keeps talking about.

Why This Conversation Even Matters

Student debt in America isn’t a niche problem anymore. It’s a structural one. The average federal borrower owes close to $40,000. Add private loans, and the national total balloons past $128 billion.

But here’s the twist. Debt itself isn’t the enemy. Debt without a matching paycheck is.

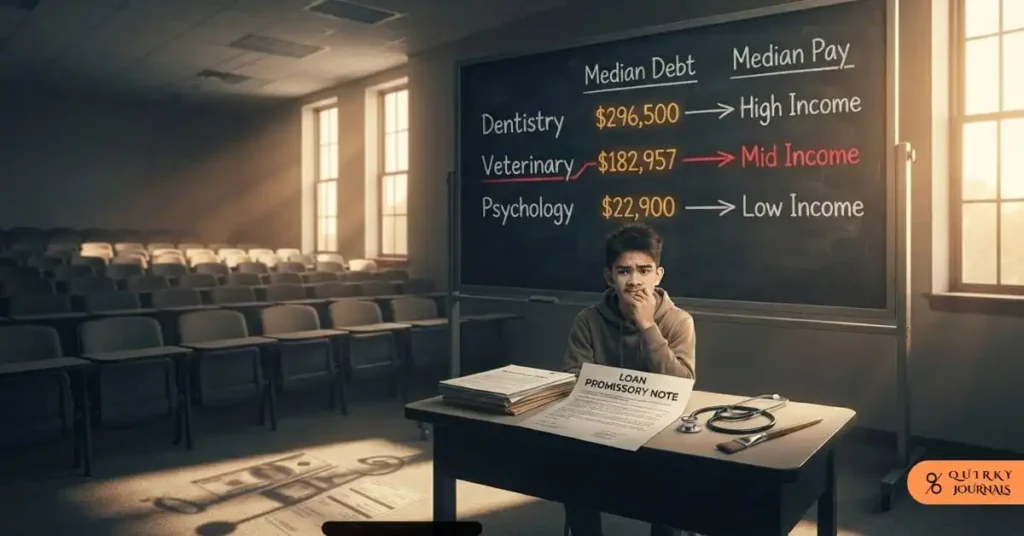

A dentist carrying $296,500 in loans is in a fundamentally different position than a psychology major carrying $22,900. One has an income trajectory that swallows the debt. The other might not.

So we need to talk about two numbers together, always. Debt load. And earning power. Never just one.

The Framework We’ll Use

Throughout this piece, we’ll rank majors using a simple lens:

- Debt Load: What’s the median amount borrowed

- Debt-to-Earnings Ratio: How long would it realistically take to pay that off

- Career Flexibility: Can you pivot if the first job doesn’t work out

This isn’t about shaming any field. Art history matters. Social work matters. But you deserve to walk in with eyes open, not blindsided at graduation.

The Heavy Hitters: Professional Degrees

Let’s start with the obvious offenders. Professional and doctoral programs dominate the top of every debt list, and for good reason. They’re expensive to run, and lenders know graduates will eventually earn enough to repay.

Dental and Medical Programs

Dental school tops nearly every ranking. Graduates leave owing an average of $296,500, and roughly 82% take out loans to get there.

Medical degrees aren’t far behind. The average new doctor graduates owing $216,659, with about 70% of the 2025 graduating class carrying some form of education debt.

Here’s the thing, though. Doctors and dentists also command some of the highest lifetime earnings of any profession. The Bureau of Labour Statistics consistently ranks these fields among the top earners in the country. The debt is brutal upfront. It’s manageable later.

| Degree | Median Debt | % Graduating With Debt |

|---|---|---|

| Dentistry | $296,500 | 82% |

| Osteopathic Medicine | $299,461 | ~70% |

| Medicine (MD) | $216,659 | 70% |

| Optometry | $193,488 | N/A |

| Veterinary Medicine | $182,957 | 83.4% |

Notice something. Veterinary medicine sits near the top of the debt chart, yet vet salaries lag well behind physician pay. That mismatch is exactly why vet students report some of the highest financial stress in any profession, according to AVMA debt surveys.

Pharmacy and Chiropractic

Pharmacy graduates aren’t spared either. The average debt stands at around $167,711, with over 82% borrowing to get through school.

Chiropractic care is a quieter surprise. Graduates owe a median of $207,635, yet chiropractor salaries rarely match those of an MD or dentist. This is where the ratio matters more than the raw number.

The Silent Debt Traps: Master’s and Advanced Degrees

MBAs get a lot of press for their price tags. And rightfully so. The average MBA graduate leaves owing $76,996. But according to Brookings research, MBA programs alone account for 4.3% of all student debt nationally, despite representing just 2.6% of borrowers.

Why? High tuition. High borrowing per student. That’s the combination that inflates the total.

The five degrees responsible for the most aggregate student debt nationally are MBA, JD, BA in Business, BS in Nursing, and MD, according to Brookings analysis of Department of Education Scorecard data.

The PhD Trap Nobody Warns You About

Here’s a stat that should get more attention. PhD graduates in Pharmacy, Pharmaceutical Sciences, and Administration post the highest median debt of any doctoral field, at $322,885.

That’s not a typo. That’s higher than most medical degrees.

Advanced dentistry graduate programs aren’t far behind, sitting at $164,553 median debt according to the same Education Data Initiative report.

The lesson here is simple. A “graduate degree” isn’t automatically safer than a professional one. Sometimes it’s worse.

Bachelor’s Degrees: Where Most Students Actually Live

Most readers aren’t headed to dental school. Let’s zoom in on undergraduate debt, since that’s where the majority of borrowers actually sit.

According to Education Data Initiative figures, the gap between the highest and lowest indebted bachelor’s majors runs about $36,905. That’s a massive swing based purely on what you choose to study.

| Bachelor’s Major | Median Debt |

|---|---|

| Registered Nursing | $80,704 |

| Communication Disorders Sciences | $90,328 |

| Clinical, Counselling, Applied Psychology | $72,287 |

| Public Health | $70,029 |

| Legal Professions (Other) | $65,254 |

| General Education | $29,134 |

Nursing: A Special Case Worth Studying

Nursing deserves its own section because the debt scales dramatically with degree level.

- Associate Degree in Nursing (ADN): $23,302

- Bachelor of Science in Nursing (BSN): $28,917

- Master of Science in Nursing (MSN): $49,047

Almost 70% of nursing students take out loans, per SoFi’s data breakdown. But nursing also boasts one of the strongest job markets in the country right now. The BLS projects steady growth through the decade, which softens the blow considerably.

Architecture: Underrated Debt Burden

Architecture flies under the radar in most debt conversations, but it shouldn’t. Bachelor’s graduates owe an average of $27,539, and that climbs to $41,398 at the master’s level.

Combine that with notoriously slow early-career salary growth in architecture firms, and you get a debt-to-income ratio that stings longer than most students expect.

The Majors Where Debt Doesn’t Pay Off

Now for the uncomfortable part. Some majors carry moderate debt but produce genuinely weak earning outcomes. This is where the ratio, not the raw dollar figure, tells the real story.

Brookings data flags several standouts here. Nearly 3% of all graduates carrying debt hold degrees in cosmetology, where average earnings sit around $16,600 against roughly $9,900 in debt. Small numbers, sure. But the ratio is punishing relative to income.

Psychology majors show up too. About 3.3% of debt-holding graduates carry a BA in Psychology, with typical earnings barely above a high school graduate’s, roughly $28,400, against a $22,900 median debt load.

Arts Majors and the Career Detour Problem

Here’s a finding that deserves more attention than it gets. Research published in a peer-reviewed study on arts graduates found that debt actively changes career paths, not just finances.

Arts majors carrying $50,000 or more in debt are roughly 17% less likely to work in jobs related to their field, compared to arts majors with lighter debt loads. Debt doesn’t just cost money. It narrows your options.

That’s worth sitting with. The loan isn’t just a bill. It’s a force that pushes people away from the exact career their degree prepared them for.

Why Similar Majors Produce Wildly Different Debt Loads

You might be wondering why two students in the same major graduate with different debt totals. A few factors drive this consistently.

School Selection

Private universities and out-of-state tuition inflate borrowing dramatically. The same nursing degree can cost half as much at a state school compared to a private institution.

Program Length

Extra years mean extra loans. Five-year architecture programs or extended nursing tracks naturally accumulate more debt than standard four-year paths.

Borrowing Behavior

Federal loans cap out at fairly modest annual limits. Once students hit that ceiling, private loans fill the gap, often at higher interest rates and with fewer protections.

According to Hamilton Project research, median debt across most majors actually clusters between $24,000 and $27,000. The extremes we’ve discussed sit far outside that norm, driven mostly by professional and doctoral programs.

How to Actually Use This Information

Data is only useful if it changes a decision. Here’s how to apply it.

Run the Ratio, Not Just the Total

A $150,000 debt load attached to a $200,000 starting salary is manageable. The same debt attached to a $45,000 salary is a crisis. Always calculate debt as a percentage of expected first-year income.

Check Completion Rates, Not Just Enrollment

Programs with high dropout rates often leave students with debt and no degree at all, the worst possible outcome. Look up College Scorecard completion data before committing.

Ask About Loan Forgiveness Paths

Fields like nursing, public health, and education sometimes qualify for Public Service Loan Forgiveness. That single factor can flip a bad debt-to-income ratio into a good one.

Consider Community College Transfer Paths

Starting at a community college and transferring can shave tens of thousands off total debt, especially for majors where the first two years are largely general education anyway.

A Quick Gut-Check Table Before You Commit

| Question | Why It Matters |

|---|---|

| What’s the median debt for this exact program at this exact school? | National averages hide massive institutional variance |

| What do graduates earn in year one, third, and five? | Early earnings often understate the long-term trajectory |

| Does this field have forgiveness or repayment assistance programs? | Can dramatically change the real cost of the debt |

| What’s the completion rate for this specific program? | Debt without a degree is the worst outcome possible |

The Bigger Picture on Student Debt

Zoom out far enough, and a pattern emerges. It’s rarely the debt amount alone that determines financial hardship. It’s the mismatch between debt and earning power.

Law degrees average $130,000 in debt, yet 71% of grads borrow to get there, and most eventually land salaries that make that number manageable.

Compare that to an associate degree in liberal studies, where Brookings notes typical debt sits around $13,000 against earnings of just $24,670. Smaller numbers on paper. Rougher math in practice.

Neither extreme should scare you off entirely. But both demand the same homework before enrollment: check the ratio, not just the sticker price.

Spend some time for your future.

To deepen your understanding of today’s evolving financial landscape, we recommend exploring the following articles:

The Smart Financial Plan: Order of Operations That Actually Works

6 Broke-to-Billionaire Stories and the Habits That Made Them

Why the Coming AI Crash Will Make the Global Financial Crisis Look Easy

The Real Reason Half of Millennials Still Take Money From Mom and Dad

Explore these articles to get a grasp on the new changes in the financial world.

Legal Disclaimer

This article is provided for general informational and educational purposes only and does not constitute financial, legal, or career advice. Student loan debt figures cited are based on aggregated third-party research and may vary by institution, program, graduation year, and individual borrower circumstances. Readers should consult a qualified financial advisor, their institution’s financial aid office, or the U.S. Department of Education before making borrowing decisions. The author and publisher assume no liability for decisions made based on the information presented here.

References

- SoFi, “What Majors Have the Highest Student Loan Debt?” [Online]. Available: https://www.sofi.com/learn/content/student-debt-by-majors

- A. Chingos and B. Akers, “Dept. of Education’s College Scorecard shows where student loans pay off and where they don’t,” Brookings Institution. [Online]. Available: https://www.brookings.edu/articles/ed-depts-college-scorecard-shows-where-student-loans-pay-off-and-where-they-dont

- Education Data Initiative, “Student Loan Debt by Major,” 2026. [Online]. Available: https://educationdata.org/student-loan-debt-by-major

- The Hamilton Project, “Major Decisions: Graduates’ Earnings Growth and Debt Repayment,” Brookings Institution. [Online]. Available: http://www.hamiltonproject.org/assets/files/major_decisions_graduates_earnings_growth_debt_repayment.pdf

- PMC, “Student loan debt and the career choices of college graduates with majors in the arts,” National Centre for Biotechnology Information. [Online]. Available: https://pmc.ncbi.nlm.nih.gov/articles/PMC10017337

- U.S. Bureau of Labour Statistics, “Occupational Outlook Handbook.” [Online]. Available: https://www.bls.gov/ooh/

- Federal Student Aid, U.S. Department of Education. [Online]. Available: https://studentaid.gov/

- U.S. Department of Education, “College Scorecard.” [Online]. Available: https://collegescorecard.ed.gov/