Retirement Calculator Formula: How to Estimate Your Future Needs

Planning for retirement is one of the most important financial decisions you will ever make. Yet many people put it off because they are not sure where to begin. The good news is that a solid retirement calculator formula can help you cut through the confusion and figure out exactly what you need to save.

Retirement planning does not have to be complicated. Once you understand the core formula and the key variables involved, you can build a plan that actually works. This guide will walk you through everything you need to know, from the basic math to the tools that make it easier.

Whether you are just starting in your career or already approaching your final working years, understanding your retirement savings goals is essential. Let us break it all down step by step.

Why You Need a Retirement Calculator Formula

Many people guess at how much they need to retire. Unfortunately, guessing rarely works. Without a structured formula, you risk either under-saving or over-saving, both of which create problems.

Under-saving is obviously dangerous. Running out of money in retirement is a real possibility if you do not plan carefully. On the other hand, over-saving means sacrificing quality of life during your working years when you could have enjoyed more financial freedom.

A proper retirement income formula balances these two risks. It accounts for inflation, investment returns, your expected lifespan, and your lifestyle goals. Moreover, it gives you a clear target to work toward, which makes consistent saving much easier.

According to NerdWallet, their retirement calculator factors in salary increases, compound interest, inflation, and rates of return to estimate what you will need. That kind of detail is exactly why a formula-based approach beats guessing every time.

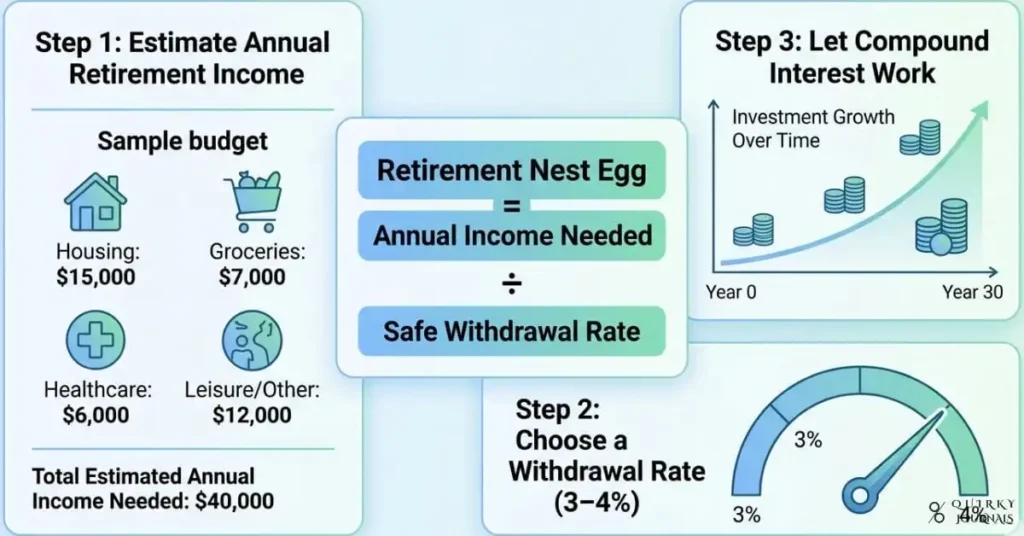

The Core Retirement Calculator Formula Explained

At its heart, the retirement formula answers one key question: how much money do you need saved on the day you retire? The answer depends on three things: how much annual income you need, how many years you expect to be retired, and what return your savings will earn.

The basic formula looks like this:

Retirement Nest Egg = Annual Retirement Income Needed / Safe Withdrawal Rate

For example, if you need $60,000 per year and you use a 4% safe withdrawal rate, you divide $60,000 by 0.04. That gives you $1,500,000 as your retirement savings target.

This approach, known as the 4% rule, is widely used among financial planners. It suggests that you can withdraw 4% of your portfolio each year without running out of money over a 30-year retirement. However, keep in mind that this is a guideline, not a guarantee.

Furthermore, you can adjust the withdrawal rate based on your risk tolerance. A more conservative approach uses 3%, while a more aggressive one might use 5%. Each choice changes your savings target significantly.

Estimating Your Annual Retirement Income Needs

Before you can use the formula, you need to know your annual retirement income target. Several methods help you figure this out, and each has its own advantages.

The Percentage-of-Income Method

The most common approach is to target a percentage of your current pre-retirement income. First National Bank explains that this percentage typically ranges from 60% to 90%, depending on your expected lifestyle.

For instance, if you currently earn $80,000 per year, targeting 70% means planning for $56,000 annually in retirement. This figure assumes that certain expenses will disappear, such as payroll taxes, commuting costs, and work-related clothing.

However, this method has limits. It does not account for your individual spending habits or any major lifestyle changes you plan to make. Therefore, use it as a starting point rather than a final answer.

The Budget-Based Method

A more precise approach involves building a detailed retirement budget. List all your expected expenses in retirement, including housing, healthcare, food, travel, and entertainment. Then add them up to find your annual need.

This method takes more effort, but it produces more accurate results. It also forces you to think carefully about what your retirement lifestyle will actually look like.

According to UMCU’s retirement savings calculator, you should aim for 70% to 80% of your pre-retirement income, but you can adjust based on your expected lifestyle and expenses. That flexibility is important because everyone’s retirement looks different.

Table 1: Income Replacement Rate Comparison

|

Lifestyle Type |

Replacement Rate |

Example Income |

Annual Need |

|

Frugal |

60% |

$70,000 |

$42,000 |

|

Moderate |

70-75% |

$70,000 |

$49,000-$52,500 |

|

Comfortable |

80% |

$70,000 |

$56,000 |

|

Luxurious |

90%+ |

$70,000 |

$63,000+ |

How Compound Interest Powers Your Retirement Savings

Compound interest is the single most powerful force in retirement savings. It means your money earns returns, and then those returns earn more returns. Over the decades, this effect has become enormous.

Consider a simple example. If you invest $10,000 today at a 7% annual return, it grows to roughly $76,000 in 30 years. Without compounding, you would only have $31,000. That difference of $45,000 comes entirely from reinvested earnings.

The key to maximising compound interest is starting early. Even small contributions in your 20s can outperform much larger contributions made in your 40s. This is why financial experts consistently recommend saving as early as possible.

Furthermore, the frequency of compounding matters. Daily compounding produces slightly better results than annual compounding. Most retirement accounts compound either daily or monthly, which works in your favour over time.

Accounting for Inflation in Your Retirement Plan

Inflation is a silent threat to retirement savings. Over time, it erodes the purchasing power of your money. Something that costs $1 today might cost $2 or more in 30 years.

According to Bankrate’s retirement calculator, from 1925 through 2024, the Consumer Price Index (CPI) averaged about 3.0% annually. Over the last 50 years, the highest CPI recorded was 13.5% in 1980. These numbers show that inflation is real and must be factored into any retirement plan.

To adjust for inflation, you need to increase your retirement income target each year. Most retirement planning tools default to a 2.3% to 3% inflation rate. You can adjust this figure based on your expectations.

Additionally, consider that healthcare costs tend to rise faster than general inflation. Medical expenses in retirement can be substantial. Therefore, planning for healthcare separately from your general budget is a smart move.

Table 2: Impact of Inflation on Purchasing Power Over Time

|

Years |

Inflation Rate |

Today’s $50,000 |

Equivalent Future Need |

|

10 years |

2.3% |

$50,000 |

$62,700 |

|

20 years |

2.3% |

$50,000 |

$78,600 |

|

30 years |

2.3% |

$50,000 |

$98,600 |

|

30 years |

3.0% |

$50,000 |

$121,400 |

Choosing the Right Retirement Age

When you plan to retire has a massive impact on how much you need to save. Retiring early means more years of retirement to fund and fewer years of contributions. Retiring later means fewer retirement years and more time to build your nest egg.

Most retirement calculators default to age 67 as the full retirement age for Social Security. This is the age at which most people receive their maximum benefit. However, your personal target may differ based on health, finances, and lifestyle goals.

According to First National Bank, retiring at 50 will cost significantly more than retiring at 65. Every extra year of retirement means one more year of expenses and one less year of savings growth. Both effects compound over time.

Conversely, delaying retirement even a few years can dramatically improve your financial position. Working until 70 instead of 65, for example, gives you five more years of contributions, five more years of investment growth, and reduces the number of years your savings must last.

Table 3: Retirement Age vs. Required Savings (Assuming $60,000/year need, 4% withdrawal rate)

|

Retirement Age |

Life Expectancy |

Years in Retirement |

Savings Target |

|

55 |

85 |

30 years |

$1,500,000 |

|

62 |

85 |

23 years |

$1,500,000 |

|

67 |

85 |

18 years |

$1,500,000 |

|

70 |

85 |

15 years |

$1,350,000 |

Note that the 4% rule assumes a 30-year retirement. If you retire early and expect 35 or 40 years in retirement, you may need a lower withdrawal rate and a larger savings target.

Understanding the Role of Social Security

Social Security is an important piece of the retirement income puzzle. However, it is rarely enough on its own. You should think of it as a supplement to your personal savings, not a replacement for them.

Your Social Security benefit depends on your earnings history and the age at which you claim. Claiming at 62 gives you a reduced benefit. Waiting until 70 gives you the maximum benefit, which can be 32% more than the full retirement age amount.

The Merrill Edge retirement calculator uses wage growth projections from the Social Security Administration (SSA) to estimate your benefit. This helps you see how Social Security fits into your overall plan.

Importantly, you should subtract your expected Social Security income from your total retirement income need before calculating your savings target. This reduces the amount you must save on your own.

For example, if you need $60,000 per year and expect $18,000 from Social Security, your savings must cover $42,000. Using the 4% rule, that means a savings target of $1,050,000 rather than $1,500,000. That is a significant difference.

How Much Should You Save Each Month?

Once you know your retirement savings target, the next step is working backwards to find your required monthly contribution. Several factors influence this number, including your current savings, your expected investment returns, and how many years you have until retirement.

Experts generally recommend saving 10% to 15% of your pretax income for retirement. However, if you are starting late, you may need to save considerably more to catch up.

A retirement savings growth calculator can quickly show you the monthly contribution needed, given your inputs. Simply enter your current age, retirement age, current savings, expected return, and savings target. The calculator does the math for you.

Moreover, consistency is crucial. Making regular contributions every month, regardless of market conditions, is one of the most reliable paths to long-term wealth. This approach, called dollar-cost averaging, reduces the impact of market volatility on your portfolio.

Employer Matching: Free Money You Should Not Leave Behind

If your employer offers a 401(k) match, contributing enough to capture the full match is essentially a 100% instant return on your money. This is one of the best deals in personal finance and should always be your priority.

For instance, if your employer matches 50% of contributions up to 6% of your salary, and you earn $70,000 per year, contributing 6% ($4,200) gets you an additional $2,100 from your employer. Over 30 years, that match alone can grow to well over $200,000.

Therefore, always factor employer contributions into your retirement savings calculation. They meaningfully reduce the amount you need to save.

Using a Retirement Calculator: Step-by-Step

Online retirement calculators take the complex math off your plate. However, knowing what inputs to use makes a big difference in the accuracy of your results.

Step 1: Enter Your Current Age and Retirement Age

Your current age determines how many years you have to save. Your target retirement age sets the length of your savings window. Together, these numbers define the foundation of your calculation.

As UMCU explains, the more years you have to save, the more your investments can grow through compound interest. Even a few extra years can make a substantial difference.

Step 2: Input Your Current Savings

Enter the total current value of all your retirement accounts. This includes your 401(k), IRA, Roth IRA, and any other retirement investments. This figure is your starting point.

Do not overlook smaller accounts or old employer plans. Every dollar in your existing savings reduces the amount you need to contribute in the future.

Step 3: Set Your Expected Investment Return

Most calculators default to a 6% to 7% average annual return. This figure is based on historical stock market performance, adjusted downward to account for a balanced portfolio that includes bonds.

Keep in mind that future rates of return cannot be predicted with certainty. Therefore, using a conservative return estimate reduces the risk of falling short of your savings target.

Step 4: Account for Inflation

Most calculators include an inflation field. Use a rate between 2% and 3% for general planning. Adjust upward if you expect higher healthcare or housing costs in your retirement years.

Step 5: Enter Your Monthly Contribution

Input what you currently save each month across all retirement accounts, including employer matches. If you are not yet saving, enter zero and use the results as motivation to start.

The calculator will then show you whether you are on track and what adjustments you might need to make.

Table 4: Key Retirement Calculator Inputs and What They Mean

|

Input |

Why It Matters |

Default/Typical Value |

|

Current Age |

Sets savings window |

Your actual age |

|

Retirement Age |

Defines retirement length |

67 years old |

|

Current Savings |

Starting point for growth |

Total of all accounts |

|

Monthly Contribution |

Drives future growth |

10-15% of income |

|

Expected Return |

Determines growth rate |

6-7% annually |

|

Inflation Rate |

Erodes purchasing power |

2.3-3% annually |

|

Income Replacement % |

Sets income target |

70-85% of income |

The 4% Rule: A Widely Used Retirement Formula

The 4% rule is one of the most cited guidelines in retirement planning. It originated from the Trinity Study, a 1998 research paper that examined historical portfolio survival rates. The study found that a portfolio could sustain a 4% annual withdrawal for at least 30 years in most historical scenarios.

Using this rule is simple. Multiply your annual retirement income need by 25. That gives you your savings target. For example, $50,000 x 25 = $1,250,000. Alternatively, divide by 0.04 to get the same result.

However, the 4% rule has critics. Some financial planners argue that in today’s low-interest environment, a 3% to 3.5% rate is safer. Others feel comfortable with 4.5% if they have flexible spending habits.

Additionally, the rule assumes a specific portfolio mix of 50% to 75% stocks. If your portfolio is more conservative, your sustainable withdrawal rate might be lower. Therefore, treat the 4% rule as a useful starting point rather than an absolute truth.

Common Mistakes People Make With Retirement Formulas

Even with the right tools, many people make avoidable mistakes when planning for retirement. Being aware of these pitfalls helps you avoid them.

Underestimating Life Expectancy

People consistently underestimate how long they will live. According to First National Bank, life expectancies are on the rise. Running out of money in your 80s is a real risk if you plan for only 20 years of retirement.

Instead, plan for at least 25 to 30 years of retirement. If you retire at 65, plan to age 90 or 95. This conservative approach provides a safety cushion.

Ignoring Healthcare Costs

Healthcare is one of the largest expenses in retirement. Many people forget to budget for it. Medicare does not cover everything, and out-of-pocket costs can reach tens of thousands of dollars per year.

Including a dedicated healthcare budget line in your retirement planning calculation is, therefore, highly advisable.

Not Adjusting for Salary Growth

Your income will likely grow over your career. If you base your retirement target on your current salary without adjusting for raises, you may end up with a target that is too low.

The Merrill Edge calculator assumes annual salary growth of 2.3% by default. Adjusting this figure to reflect your actual expected raises produces a more accurate target.

Counting on Inheritance or Windfalls

Basing your retirement plan on expected inheritances or other windfalls is risky. Circumstances change, and the money that you expect to receive may not materialise. Build your plan on what you can control: your own savings and contributions.

Retirement Account Types and Their Role in Your Formula

Different retirement accounts have different tax treatments, contribution limits, and withdrawal rules. Understanding each type helps you optimise your overall savings strategy.

Traditional 401(k) and IRA

Contributions to traditional 401(k) and IRA accounts are made with pre-tax dollars. This means you get a tax break today, but you pay taxes when you withdraw in retirement. These accounts are great for people who expect to be in a lower tax bracket in retirement.

For 2024, the 401(k) contribution limit is $23,000 for those under 50. Workers aged 50 and over can contribute an additional $7,500 as a catch-up contribution.

Roth 401(k) and Roth IRA

Roth accounts use after-tax contributions. You pay taxes now, but your money grows tax-free and qualified withdrawals in retirement are not taxed. Roth accounts are particularly valuable if you expect to be in a higher tax bracket in retirement.

Including a mix of traditional and Roth accounts in your retirement savings plan gives you tax flexibility in retirement. This approach is known as tax diversification.

SEP IRA and Solo 401(k) for Self-Employed Individuals

If you are self-employed, you have access to retirement accounts with much higher contribution limits. A SEP IRA allows contributions of up to 25% of net self-employment income. A Solo 401(k) has the same limits as a regular 401(k) but also includes an employer contribution component.

These accounts make it possible for self-employed individuals to save large amounts quickly. Consulting a financial advisor to choose the best option for your situation is a worthwhile investment.

How Investment Returns Affect Your Retirement Formula

Your expected investment return is one of the most important variables in the retirement formula. Small differences in return rates lead to dramatically different outcomes over decades.

For example, $200,000 invested for 30 years at 5% grows to about $865,000. At 7%, it grows to about $1,520,000. That is a difference of over $650,000 from just a 2% change in the annual return.

This is why choosing the right asset allocation matters so much. A portfolio that is too conservative may not grow fast enough. One that is too aggressive may expose you to excessive volatility close to retirement.

The general rule of thumb is to subtract your age from 110 to determine the percentage of stocks in your portfolio. At age 40, for example, you might hold 70% stocks and 30% bonds. As you age, you gradually shift toward more conservative holdings.

Table 5: Investment Return Rate Impact on $200,000 Over 30 Years

|

Annual Return |

Value After 30 Years |

Additional Growth vs. 4% |

|

4% |

$648,680 |

Baseline |

|

5% |

$864,388 |

+$215,708 |

|

6% |

$1,148,698 |

+$500,018 |

|

7% |

$1,522,451 |

+$873,771 |

|

8% |

$2,009,661 |

+$1,360,981 |

Adjusting Your Retirement Formula Over Time

Your retirement formula is not a set-it-and-forget-it calculation. Life changes, markets fluctuate, and your goals evolve. Revisiting your plan regularly is essential for staying on track.

Most financial advisors recommend reviewing your retirement plan at least once a year. Additionally, major life events such as marriage, divorce, a new job, or having children should trigger an immediate review.

When you review your plan, update all the key variables: your current savings balance, expected contributions, estimated Social Security benefit, and retirement income target. Then use a retirement calculator to see whether you are still on track.

Moreover, as you approach retirement, shift your focus from accumulation to preservation. Gradually reducing risk in your portfolio helps protect the wealth you have built.

Early Retirement: Adjusting the Formula for FIRE

The FIRE movement, which stands for Financial Independence, Retire Early, takes the retirement formula to an extreme. Followers of this approach aim to retire in their 30s or 40s by saving aggressively and living frugally.

For FIRE, the standard 4% rule is often considered too aggressive. With 40 or 50 years of retirement ahead, a 3% or even 3.5% withdrawal rate is more appropriate. This means saving 33 to 40 times your annual expenses rather than 25 times.

Additionally, FIRE followers often rely heavily on Roth IRA ladders and taxable brokerage accounts to access funds before the traditional retirement account age of 59.5 without penalties.

This approach requires significant discipline and sacrifice during the saving years. However, for those who value freedom and flexibility over material consumption, it can be a highly rewarding path.

Tools and Resources to Help You Calculate Retirement Needs

Several excellent tools are available to help you run the retirement formula without doing the math yourself. Each has slightly different features and assumptions.

The NerdWallet retirement calculator is one of the most user-friendly options available. It accounts for salary increases, compound interest, inflation, and rates of return. The interface is clean and easy to navigate.

Additionally, Bankrate’s retirement plan calculator calculates year-by-year withdrawals through age 95. This is particularly useful for modelling scenarios where you expect variable spending in retirement.

The Merrill Edge personal retirement calculator generates two scenarios: average market performance and poor market performance. Seeing the worst-case scenario helps you understand the risk in your plan.

Finally, UMCU’s retirement savings growth calculator is excellent for modelling how consistent monthly contributions grow over time. It clearly shows the impact of compound interest in a visual and easy-to-understand format.

Making Your Retirement Plan Inflation-Proof

Beyond adjusting your income target for inflation, there are specific strategies you can use to make your retirement portfolio more inflation-resistant.

First, consider holding a portion of your portfolio in Treasury Inflation-Protected Securities, or TIPS. These bonds automatically adjust their principal based on the CPI. They provide a reliable hedge against rising prices.

Second, real estate can be a powerful inflation hedge. Property values and rental income tend to rise with inflation over time. A real estate investment trust, or REIT, allows you to gain this exposure without the hassle of being a landlord.

Third, dividend-paying stocks in sectors like consumer staples and utilities tend to hold up well during inflationary periods. Companies with strong pricing power can pass cost increases on to consumers, protecting their profit margins and dividends.

Together, these strategies can help ensure that your purchasing power remains intact throughout a long retirement. Consulting a certified financial planner can help you design the right mix for your situation.

Sample Retirement Formula Calculation: A Practical Example

Let us walk through a complete example to bring all the concepts together.

Sarah is 35 years old and earns $85,000 per year. She plans to retire at 67 and expects to live to 90. She currently has $45,000 saved in her 401(k) and contributes $500 per month, including her employer match. She expects a 7% annual return and uses a 2.5% inflation rate.

First, we calculate her annual retirement income need. She targets 75% of her pre-retirement income. Adjusting $85,000 for 32 years of inflation at 2.5%, her salary at retirement will be approximately $185,000. Seventy-five per cent of that is $138,750 per year.

Next, she estimates her Social Security benefit at $22,000 per year (in today’s dollars, adjusted for inflation). Subtracting this from $138,750 leaves $116,750 needed from her savings annually.

Using the 4% rule: $116,750 / 0.04 = $2,918,750 savings target.

Finally, using a retirement savings calculator, she finds that $45,000 growing at 7% for 32 years, plus $500 per month, gives her approximately $2,400,000. She is somewhat short of her target. To close the gap, she needs to increase her monthly contribution to about $650.

This kind of concrete, step-by-step calculation is exactly what the retirement formula is designed to produce. It transforms a vague worry into a specific, actionable plan.

How to Catch Up If You Are Behind on Retirement Savings

Many people reach their 40s or 50s without having saved nearly enough for retirement. The good news is that catching up is possible, though it does require effort and commitment.

To begin with, the IRS allows catch-up contributions for workers aged 50 and over. In 2024, you can contribute an extra $7,500 to a 401(k) and an extra $1,000 to an IRA. Taking full advantage of these limits accelerates your savings significantly.

Furthermore, reducing current expenses frees up more cash for retirement contributions. Even modest lifestyle adjustments, such as eating out less or delaying a new car purchase, can translate into thousands of extra dollars saved each year.

Additionally, consider delaying retirement by even two or three years. As discussed earlier, this has a compounding positive effect: more savings time, more investment growth, fewer retirement years to fund, and higher Social Security benefits.

Finally, working with a certified financial planner can help you identify strategies specific to your situation. Personalised advice is often more valuable than general guidelines.

Final Thoughts on the Retirement Calculator Formula

Estimating your retirement needs is not a perfect science. No formula can predict the future with certainty. However, a well-constructed retirement calculator formula gives you a solid framework to work within.

The core principles are straightforward: estimate your income need, account for inflation, factor in investment returns, subtract expected Social Security income, and apply the 4% rule or your chosen withdrawal rate. Then work backwards to find your required monthly savings.

Revisiting and updating your plan regularly ensures that you stay on course as life changes. The earlier you start, the less you need to save each month thanks to the power of compound interest.

Use the calculators from NerdWallet, Bankrate, Merrill Edge, and UMCU as starting points. Each one offers slightly different features that together paint a comprehensive picture.

Above all, take action. Even an imperfect plan executed consistently beats a perfect plan that stays on paper. Your future self will thank you for every dollar saved today.

Spend some time for your future.

To deepen your understanding of today’s evolving financial landscape, we recommend exploring the following articles:

The Diversification Myth: Understanding Correlation Breakdown During Market Stress

The Startup GTM Playbook: Launching Your Product to the Right Audience

Can Samsung Win by Becoming More Like Apple?

Bitcoin’s 50% Drawdown: How the US Budget War Hit Crypto Liquidity

Explore these articles to get a grasp on the new changes in the financial world.

Disclaimer

The information in this article is provided for educational purposes only. It does not constitute financial, investment, tax, or legal advice. Retirement planning involves complex variables, and individual circumstances vary widely. Always consult a qualified financial advisor before making any retirement-related financial decisions. Past investment performance does not guarantee future results.

References

[1] NerdWallet, ‘Retirement Calculator,’ [Online]. Available: https://www.nerdwallet.com/investing/calculators/retirement-calculator. [Accessed: Mar. 2025].

[2] UMCU, ‘Retirement Savings Growth Calculator,’ [Online]. Available: https://www.umcu.org/learn/resources/calculators/save-for-retirement-calculator. [Accessed: Mar. 2025].

[3] Merrill Edge, ‘Personal Retirement Calculator,’ [Online]. Available: https://www.merrilledge.com/retirement/personal-retirement-calculator. [Accessed: Mar. 2025].

[4] First National Bank, ‘Estimating Your Retirement Income Needs,’ [Online]. Available: https://www.fnb-online.com/personal/knowledge-center/plan-for-retirement/estimating-retirement-needs. [Accessed: Mar. 2025].

[5] Bankrate, ‘Retirement Calculator: Estimate How Much You Need To Save,’ [Online]. Available: https://www.bankrate.com/retirement/retirement-plan-calculator/. [Accessed: Mar. 2025].