$1M to Bankruptcy: The Psychology That Breaks Lottery Winners

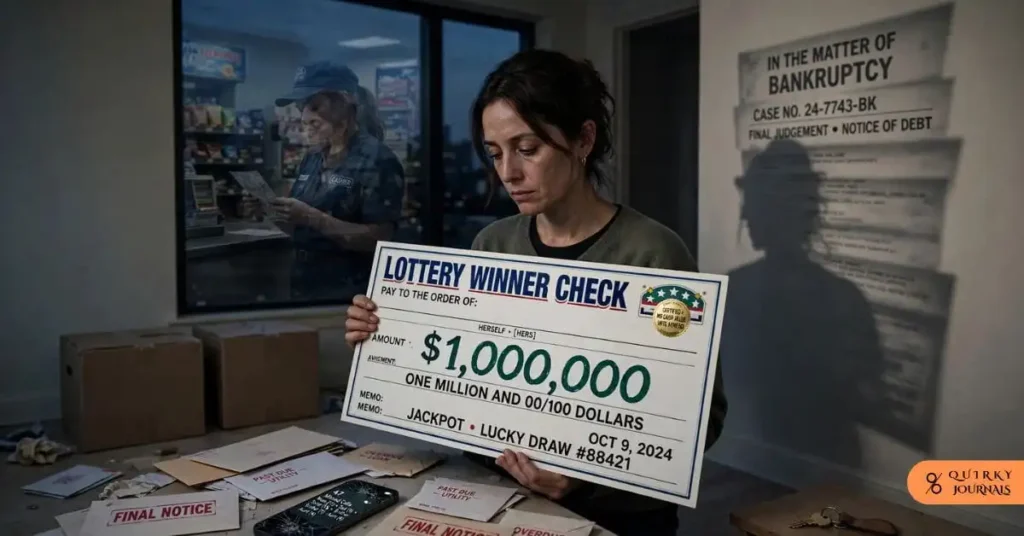

A woman in Michigan won $1 million. Eight years later, she filed for bankruptcy. This isn’t rare. It’s the norm. Roughly 70 per cent of people who receive a windfall lose it within a few years. That number should stop you cold.

We tend to assume money problems are math problems. Spend less than you earn. Save the rest. Simple, right? Except sudden wealth doesn’t behave like a math problem. It behaves like a psychological event, and most winners never see it coming.

This piece breaks down why that happens. Not the surface-level “they were bad with money” explanation. The real mechanics underneath it: identity collapse, guilt, social rupture, and a brain that simply wasn’t built to process this kind of shock.

The Myth We All Believe About Money

Ask most people what they’d do with a $10 million jackpot. They’ll describe a plan. Pay off debt. Buy a house. Help the family. Invest the rest. It sounds rational and orderly.

Here’s the problem. That plan assumes a stable, unchanged version of you will be the one executing it. But wealth doesn’t arrive quietly into a stable life. It detonates. And the person left standing after the blast is not quite the same person who bought the ticket.

Consider the timeline. A regular income earner, someone making $60,000 a year, suddenly holds $50 million. Every financial habit they built over decades becomes obsolete overnight. Meanwhile, nobody hands them a manual. There’s no onboarding process for sudden wealth, no HR department walking them through the transition.

So they improvise. And improvisation, under emotional pressure, tends to go badly.

What Sudden Wealth Syndrome Actually Is

Wealth psychologist Stephen Goldbart coined a term for this: sudden wealth syndrome. It isn’t a formal clinical diagnosis you’ll find in a diagnostic manual. Still, financial planners and therapists recognise it as a consistent, predictable pattern.

The syndrome shows up as a cluster of emotional responses. Confusion about identity. Guilt about undeserved luck. Fear that the money will vanish. Isolation from old relationships. Pressure from new ones. Each of these compounds the others, creating a feedback loop that erodes sound judgment exactly when sound judgment matters most.

The money changes almost nothing about who you are on the inside. It changes almost everything about how the world treats you. That mismatch is where the damage happens.

Notice something important here. This isn’t a character flaw. It’s a stress response, and stress responses hijack decision-making regardless of how intelligent or disciplined someone was before the windfall.

The Statistics Are Sobering

Let’s get concrete, because the numbers are worse than most people expect.

A study published in the Review of Economics and Statistics tracked 35,000 lottery winners who received between $50,000 and $150,000. Within five years, 1,900 of them had filed for bankruptcy. Florida winners specifically showed a bankruptcy rate nearly double that of non-winning residents in the same state.

It isn’t just lottery winners either. A 2015 paper in the American Economic Review found that 15 per cent of NFL players filed for bankruptcy within 12 years of retirement, despite career earnings most households will never see.

| Windfall Type | Reported Failure Rate | Timeframe |

|---|---|---|

| Lottery winners ($50k-$150k) | ~5.4% bankruptcy | 5 years |

| Florida lottery winners | ~2x baseline bankruptcy rate | Ongoing |

| Retired NFL players | 15% bankruptcy | 12 years post-retirement |

| Family wealth transfers | ~70% wealth dissipated | By the third generation |

That last row deserves attention. Even multi-generational family fortunes, built with estate planning teams and inherited financial literacy, still fail at staggering rates. Sudden wealth syndrome isn’t a lottery-specific quirk. It’s a human one.

Identity Confusion: Who Are You Now?

Your sense of self isn’t just internal. It’s built through repetition. The job you show up to. The budget you juggle. The trade-offs you make every week between wants and needs.

Remove all of that overnight, and something strange happens. You lose your reference points. Who are you if you’re not the person figuring out how to make rent? What replaces that structure?

Winners frequently describe this as disorienting rather than liberating, at least at first. According to financial psychology researchers, this identity confusion is one of the most consistent symptoms across sudden wealth cases, regardless of the amount involved.

Some people respond by clinging harder to their old identity, refusing to change anything, which can lead to strange under-spending followed by compensatory binges. Others swing the opposite direction. They adopt a new persona entirely, often modelled on media portrayals of wealthy lifestyles rather than anything sustainable.

Neither response is stable. Both stem from the same root cause: a self-concept that hasn’t caught up with a completely altered set of circumstances.

The Guilt Nobody Talks About

Here’s an uncomfortable truth. Winning the lottery is pure luck. No effort, no skill, just chance. And that randomness creates a specific kind of guilt that wealth rarely does.

Winners often report feeling like impostors. They didn’t build a company or invent a product. They bought a ticket. Meanwhile, people around them, some working brutal hours for a fraction of the payout, remain in the same financial position as before.

This guilt drives behaviour in predictable ways. Winners overcompensate. They give money away too fast, too widely, and often without proper structure, like a family trust or clear terms. Generosity is admirable. Generosity without a framework is how fortunes evaporate.

A related pattern shows up constantly in sudden wealth research: winners want to solve everyone’s financial problems simultaneously. Pay off a sibling’s mortgage. Fund a cousin’s business. Cover a friend’s medical bills. Individually reasonable. Collectively, a fast road to depletion.

Fear, Isolation, and the New Loneliness

Money is supposed to reduce stress. For many winners, it does the opposite, at least socially.

Relationships shift almost immediately after a windfall becomes public. Some friends pull away, uncomfortable with the imbalance. Others suddenly reappear, warmly, with requests attached. Distinguishing genuine connection from opportunism becomes exhausting and often impossible.

This creates a specific, isolating paradox. Winners have more resources than ever, yet fewer people they trust completely. According to wealth psychology literature, this isolation is one of the strongest predictors of poor long-term outcomes, because decisions get made without a trusted sounding board.

Fear compounds the loneliness. Winners frequently report a nagging suspicion that the money will disappear as quickly as it arrived. That anxiety, ironically, pushes some toward reckless decisions made in an attempt to “lock in” security through risky investments or big purchases, rather than patient financial planning.

The Pressure Cooker: Family, Friends, and Strangers

Once a windfall becomes known, whether through local news or word of mouth, the requests start. Family loans. Business pitches. Old acquaintances resurfacing with sudden warmth.

Winners describe this pressure as relentless. Saying no to people they love feels cruel. Saying yes to everyone is financially impossible. There’s rarely a comfortable middle ground, especially without prior experience setting financial boundaries.

This dynamic explains a counterintuitive finding from wealth management research: winners with more visible wealth, larger houses, flashier cars, often face more requests, not less. Visibility invites expectation.

Smart winners learn to build a buffer early. That usually means:

- Designating a single point of contact, often an advisor, to field requests

- Setting a fixed, pre-decided charitable or family giving budget

- Delaying major decisions for months, not days

- Keeping the full amount private wherever legally possible

None of this eliminates pressure. It does, however, create enough friction to slow down impulsive giving.

Why the Brain Isn’t Built for This

Human decision-making evolved around scarcity, not abundance. For most of history, resources were limited, and threats were immediate. Our brains developed shortcuts and cognitive biases to make fast decisions under those conditions.

Sudden wealth breaks those shortcuts. The scale is unfamiliar. The stakes feel abstract. A million dollars and a hundred million dollars can feel psychologically similar, even though the appropriate spending behaviour differs enormously.

Behavioural economists point to a specific bias at play here: present bias, the tendency to overweight immediate rewards against long-term consequences. Under normal circumstances, this bias causes minor overspending. Under sudden wealth, applied to a much larger number, it causes catastrophic overspending.

Add decision fatigue to the mix. Winners face dozens of unfamiliar, high-stakes choices in a short window, including tax structuring, investment vehicles, real estate, and family requests, often without professional guidance in place yet. Fatigue erodes judgment fast, and judgment is exactly what’s needed most in that window.

The Behavioural Patterns That Wreck Fortunes

Across nearly every sudden wealth case study, the same handful of behaviours recur. Recognising them is the first defence against repeating them.

Overspending on depreciating assets. Cars, boats, and oversized homes drain capital fast and generate ongoing costs like insurance, maintenance, and property taxes.

Risky, uninformed investments. Winners often trust unfamiliar advisors or friends pitching “guaranteed” returns, without vetting credentials through resources like the CFP Board’s advisor lookup.

Hasty lending and gifting. Loans to family members, often undocumented, rarely get repaid and frequently damage the relationship anyway.

Lifestyle inflation without a ceiling. Spending scales up continuously rather than settling at a sustainable, predetermined level.

Avoiding professional help. Many winners delay hiring a fee-only financial advisor or CPA, assuming they can manage the complexity they’ve never encountered before.

Individually, each behaviour seems survivable. Together, they compound quickly, and the runway shrinks faster than most winners expect.

Case in Point: Athletes, Inheritors, and the Same Old Story

Lottery winners get the headlines, but the pattern isn’t unique to them. Professional athletes, despite years of coaching and structure, show remarkably similar bankruptcy rates.

Inheritors follow a related, if less dramatic, path. A 2012 study in the Journal of Family and Economic Issues found that people in their 20s, 30s, and 40s who received an inheritance saved only about half of it. The rest went to spending or questionable investments.

Family wealth research shows the same erosion across generations. Roughly 70 per cent of family wealth transfers fail by the third generation, according to widely cited estate planning studies. Money earned by one generation frequently disappears within two more.

The common thread across all these groups isn’t stupidity or laziness. It’s the same psychological shock, applied to different populations, producing nearly identical outcomes. That consistency should reframe how we think about this problem entirely.

The 72-Hour Rule and Other Protective Strategies

Financial advisors who specialise in windfalls often recommend a simple starting rule: do nothing significant for the first 72 hours, and ideally much longer.

No big purchases. No public announcements. No major gifts. Just breathing room, enough to let the initial shock settle before decisions get made.

From there, a slightly longer runway helps even more. Many planners suggest a full 90-day period before any irreversible financial commitment. That includes:

- Placing funds in a secure, low-risk holding account initially

- Consulting a CPA about tax obligations before anything else

- Interviewing multiple fee-only advisors, not commission-based ones

- Drafting a basic budget based on the previous lifestyle, scaled modestly

- Delaying any public disclosure of the amount where legally allowed

None of this feels exciting. It’s not supposed to. The goal during this window is stability, not optimisation.

Building a Team Before You Build a Life

One consistent difference separates winners who keep their wealth from those who lose it: the team they build early on.

A solid foundation typically includes a CPA familiar with sudden wealth taxation, a fee-only certified financial planner, an estate attorney for trust structuring, and sometimes a therapist experienced in wealth psychology specifically.

That last one surprises people. Yet given everything covered so far, identity confusion, guilt, and isolation, it makes sense. A therapist helps process the emotional shock separately from the financial decisions, preventing the two from tangling together and clouding judgment.

Vetting matters enormously here. Winners are prime targets for opportunistic advisors promising unrealistic returns. Checking credentials through FINRA’s BrokerCheck or the SEC’s advisor database isn’t optional due diligence. It’s essential.

What Actually Works: A Practical Framework

Strip away the theory, and a workable framework emerges. It’s not glamorous, but it holds up across nearly every documented success story.

| Phase | Timeframe | Primary Focus |

|---|---|---|

| Stabilization | 0-90 days | No major spending, secure funds, assemble advisory team |

| Structuring | 3-12 months | Tax planning, trust setup, modest lifestyle adjustment |

| Allocation | 1-3 years | Diversified investing, defined giving budget, and housing decisions |

| Sustainability | Ongoing | Annual reviews, spending caps, and generational planning |

Notice how slow this looks compared to the fantasy version of sudden wealth. That’s intentional. Speed is the enemy here, and patience, unglamorous as it sounds, is the single biggest predictor of long-term success.

Budgeting tools like NerdWallet’s budgeting guides or resources from the National Endowment for Financial Education offer accessible starting points, even for people managing far more money than these tools were originally designed for.

The Long Game: Turning a Windfall Into a Foundation

Money doesn’t fix psychology. It amplifies whatever’s already there, insecurities, generosity, impulsiveness, discipline, all of it, at a much larger scale.

Winners who succeed long-term tend to treat the windfall as a tool for building something durable, a foundation, a business, an education fund, rather than as permission to escape their previous life entirely. That mindset shift, from spending to building, seems to matter more than the actual dollar amount involved.

It also helps to accept an uncomfortable truth early: this will be hard. Not hard like poverty is hard, but hard in its own specific, disorienting way. Pretending otherwise, or expecting pure euphoria, sets winners up for a harder crash when the guilt, pressure, and fear inevitably show up.

The people who navigate this well aren’t the luckiest ones. They’re the ones who slow down, build a team, and treat the money with the seriousness it demands, even when everything about the moment screams to celebrate instead.

Spend some time for your future.

To deepen your understanding of today’s evolving financial landscape, we recommend exploring the following articles:

Pump and Dump in the Age of Influencers: How Financial Fraud Moved to Instagram and Discord

Buy, Borrow, Die: How the Ultra-Wealthy Avoid Taxes Legally

Algo Trading Safety Net: Risk Management for Automated Systems

AI Crash 2026: Kospi Halts, Nasdaq Slides, Chip Stocks Bleed

Explore these articles to get a grasp on the new changes in the financial world.

Disclaimer

This article is for general informational and educational purposes only. It does not constitute financial, legal, tax, or psychological advice, and should not be relied upon as a substitute for consultation with a qualified, licensed professional. Financial and psychological outcomes vary significantly by individual circumstance. Readers experiencing a windfall event should consult a certified financial planner, CPA, estate attorney, and, where appropriate, a licensed mental health professional before making significant financial decisions.

References

[1] Wikipedia contributors, “Sudden wealth syndrome,” Wikipedia, The Free Encyclopedia. [Online]. Available: https://en.wikipedia.org/wiki/Sudden_wealth_syndrome

[2] Chesapeake Financial Planning, “Sudden Wealth Syndrome: The Hidden Threat to Lottery Winners.” [Online]. Available: https://chesapeakefp.com/sudden-wealth-syndrome-lottery-winners

[3] Minster Bank, “Strategies to Avoid Sudden Wealth Syndrome.” [Online]. Available: https://www.minsterbank.com/resources/learn/blog/wealth/avoid-sudden-wealth-syndrome

[4] U.S. Bank, “Financial Windfall: How to Manage Sudden Wealth.” [Online]. Available: https://www.usbank.com/wealth-management/financial-perspectives/financial-planning/financial-windfall.html

[5] EBSCO Research Starters, “Sudden wealth strategy.” [Online]. Available: https://www.ebsco.com/research-starters/business-and-management/sudden-wealth-strategy